The legislative draft of the EU Industrial Acceleration Act (IAA), released on March 4, 2026, consolidates local manufacturing requirements, low-carbon standards, and investment conditions into a unified regulatory framework for the first time. For Chinese enterprises looking to expand their footprint in Europe, this marks a structural shift: the traditional “export first, localize later” model is rapidly losing viability. The window to proactively realign business strategies and operational footprints is narrowing faster than many had anticipated.

This article provides a structured analysis of the IAA’s core mechanisms and policy intent, together with practical, strategy-led recommendations for Chinese enterprises seeking to operate and compete effectively in the European market.

Policy Background: Manufacturing Reindustrialization and Supply Chain Strengthening

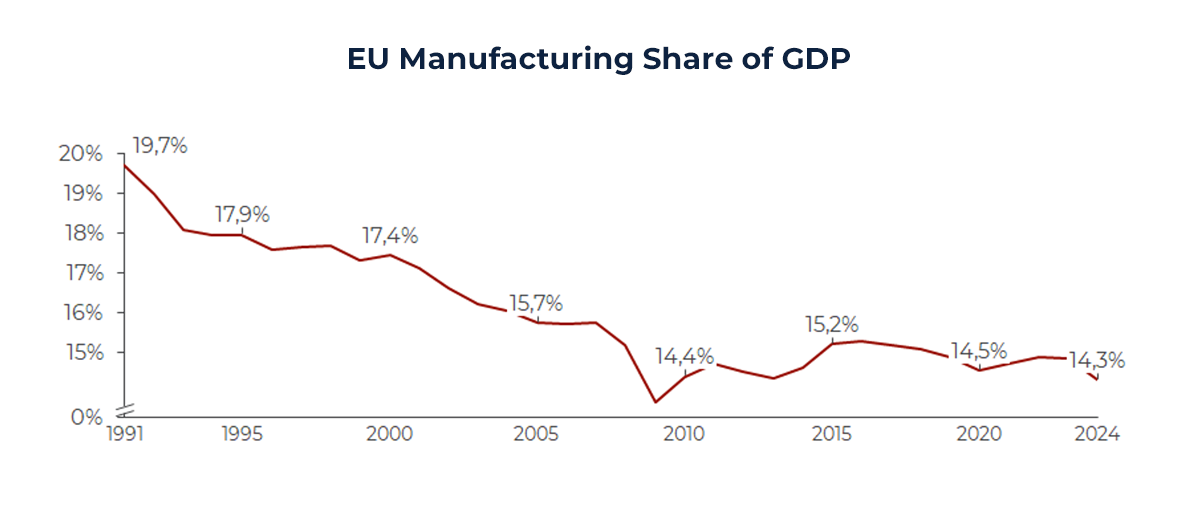

The EU plans to increase the share of manufacturing in GDP from approximately 14.3% to 20% by 2035.

To achieve this goal, several policy instruments have been successively introduced in recent years:

- December 2022, Foreign Subsidies Regulation (FSR): Strengthens scrutiny of non-EU subsidies and increases transaction compliance costs.

- June 2022, International Procurement Instrument (IPI): Restricts certain public procurements, affecting market access for non-EU companies.

- December 2022, Anti-Coercion Instrument (ACI): Prevents economic coercion and applies across multiple sectors.

- May 2024, Critical Raw Materials Act (CRMA): Reduces external dependence and imposes institutional requirements on supply chains.

- March 2026, Industrial Acceleration Act (IAA): For the first time, systematically incorporates localization, low-carbon standards, investment conditions, and approval optimization into EU policy.

Core Mechanisms of the IAA: Three Key Policy Requirements

Before discussing the specific policy requirements of the IAA, a more fundamental question merits priority attention: whether enterprises from mainland China are eligible to participate in EU public procurement at all.

The IAA explicitly stipulates that bidders owned or controlled by third-country enterprises that have not signed relevant international agreements with the EU will be excluded from EU public procurement eligibility. Since mainland China is currently not a member of the WTO Government Procurement Agreement (GPA), Chinese enterprises and their EU subsidiaries are, in principle, ineligible to participate in EU public tenders covered by the IAA.

Current formal GPA members are mainly developed economies, including the EU (all 27 member states including Spain), the United States, the United Kingdom, Canada, Japan, South Korea, Australia, and Singapore. Turkey is currently only an observer, not a formal member. Among major Southeast Asian countries, except for Singapore, Malaysia, Thailand, Vietnam, and Indonesia have not joined. This means that some enterprises previously considering entering the EU procurement market via Turkey or Southeast Asian factories (excluding Singapore) will face uncertainty regarding eligibility under the IAA framework.

This restriction is stricter than previous precedents: historically, Chinese enterprises could participate in procurement through their EU subsidiaries; the IAA extends this restriction to local EU subsidiaries, making it a critical variable for reassessing investment structures in Europe.

Given this premise, the discussion of the following three policy requirements mainly applies to enterprises that have obtained eligibility through compliant pathways.

1. Low-Carbon Standards

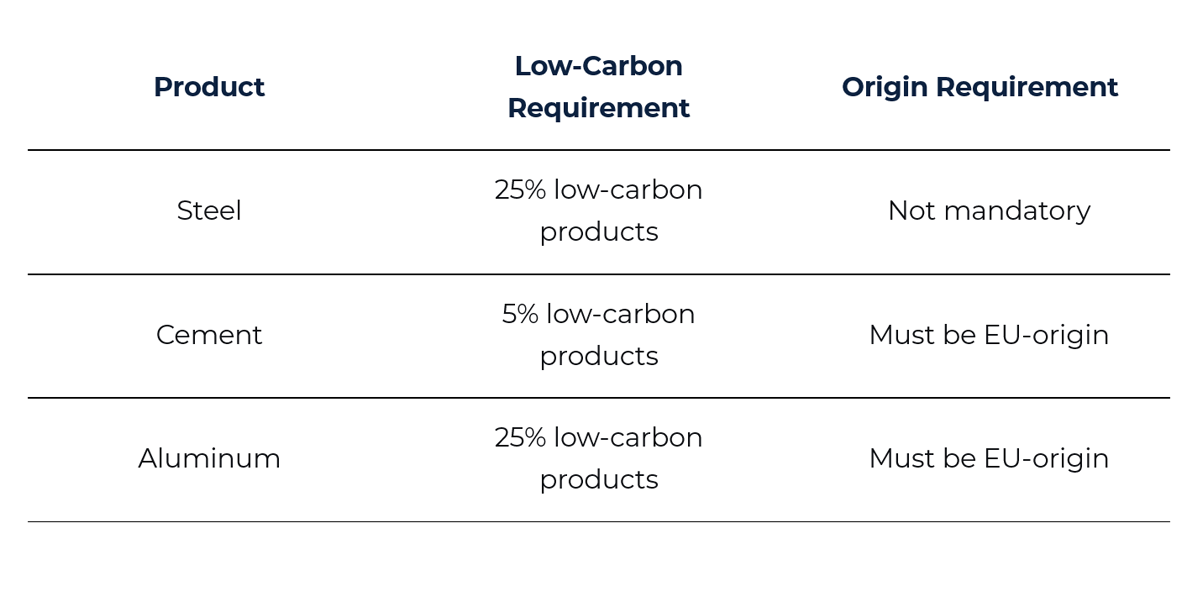

From 2029, certain industrial products participating in EU public procurement must meet low-carbon requirements. Compared with current rules, voluntary green standards are now mandatory thresholds uniformly applicable to the EU public procurement market.

For the automotive industry, aluminum’s dual thresholds (low-carbon + EU origin) are particularly impactful—aluminum is a core material for vehicle lightweighting, and compliance costs across the supply chain will increase.

Strategic Tip: Enterprises need to evaluate the low-carbon certification and compliance capabilities of existing factories and supply chains, and plan upgrades and certifications in advance.

2. Supply Chain Localization

The new energy industry chain is a key focus:

- EV components excluding batteries: To participate in public procurement or receive government subsidies, at least 70% must be manufactured in the EU.

This is the EU’s first hard threshold at the procurement level. Currently, there are no direct restrictions for consumers purchasing cars privately, but if member states tie subsidies to “EU-made” eligibility, the impact extends beyond public procurement.

- Compared with current anti-subsidy frameworks, the IAA’s localization threshold is significantly stricter: Previously, eliminating a 20.7% anti-subsidy tax required Chinese components value <60% or local value-added ≥25%, and eliminating a 10% MFN tariff required ≥45%; under the IAA, 70% of components must be EU-made, and this shifts from a “tax incentive condition” to a “market access requirement.” Failing to meet the threshold results not just in paying more tax, but losing eligibility altogether. In other words, localization is no longer just a cost-optimization option but a threshold for market access

- Power batteries: The IAA currently does not impose the same mandatory origin requirement on automotive power batteries as other categories. However, energy storage batteries (BESS) are already subject to phased controls, and whether automotive batteries will follow remains worth monitoring.

Strategic Tip: Plan production layouts and partner selection in advance using a “China + Europe/third country” supply chain model to mitigate policy risks.

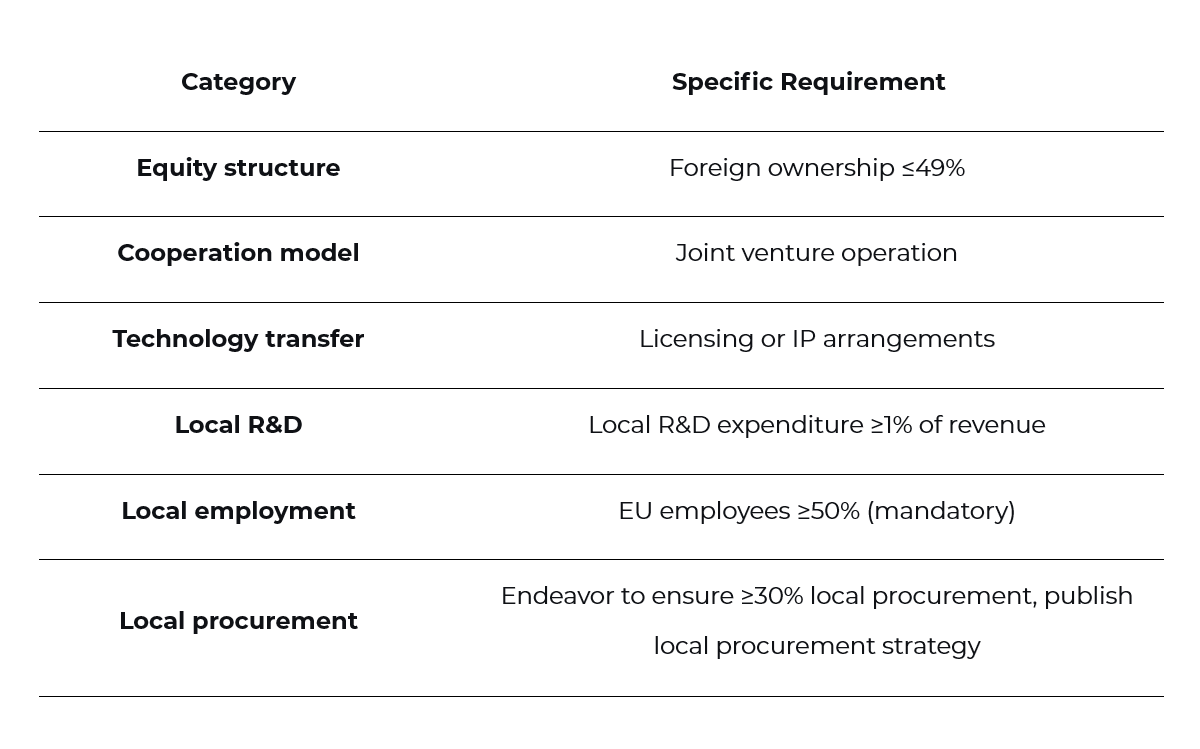

3. Investment Conditions and Industrial Cooperation

The IAA imposes additional conditions on certain foreign investment projects. The trigger thresholds are: investment exceeding €100 million, and the investor’s home country holding more than 40% of global capacity in the relevant industry. Projects meeting both thresholds must satisfy at least four of the following six conditions:

Industry Impact: Focus on Key Supply Chains

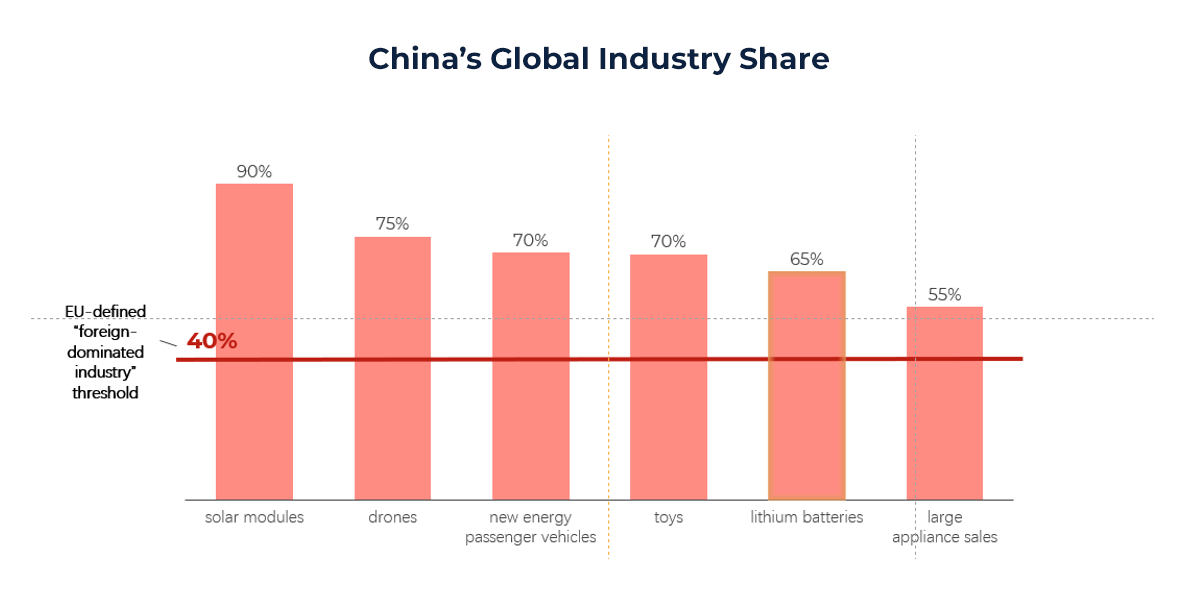

In sectors where China’s global share exceeds the EU’s “foreign-dominated industry” 40% threshold, the IAA’s FDI additional conditions will apply. In the automotive supply chain, two sectors are particularly notable: new energy passenger vehicles (≈70% global share) and lithium batteries (≈65% global share), both far exceeding the trigger threshold. This means related Chinese enterprises will face direct FDI additional condition reviews when investing in the EU.

In sectors where China’s global share exceeds the EU’s “foreign-dominated industry” 40% threshold, the IAA’s FDI additional conditions will apply. In the automotive supply chain, two sectors are particularly notable: new energy passenger vehicles (≈70% global share) and lithium batteries (≈65% global share), both far exceeding the trigger threshold. This means related Chinese enterprises will face direct FDI additional condition reviews when investing in the EU.

Policy pressures for the automotive supply chain manifest on two levels:

- Vehicles and core components: Local manufacturing ratios, investment structure design, and compliance approval are prerequisites for EU market entry; the marginal advantage of export models continues to narrow.

- Power batteries: There is increasing pressure to centralize the supply chain in Europe; energy storage batteries are already subject to phased origin control, and future policy for power batteries should be closely tracked.

Other industries shown in the diagram – solar modules, drones, toys, large appliances—also exceed the 40% red line; the IAA’s FDI additional conditions apply, and enterprises can refer to the automotive sector’s compliance logic.

Recommendations for Chinese Automakers and Component Suppliers

From a policy trend perspective, the comprehensive cost of entering the EU automotive market is systematically rising. Existing anti-subsidy frameworks have already set clear localization thresholds for Chinese EVs, and the IAA further tightens access at the procurement level. Coupled with ongoing EU-China automotive tariff negotiations and regular enforcement of FSR, IPI, and other policy tools, compliance thresholds are expected to rise over the next 2–3 years. Localization is no longer just a cost-optimization option but a market access requirement.

Under this context, Chinese enterprises should prioritize evaluation in three directions:

- Reassess the GTM path for the European market: Traditional export sales face dual pressures of tariffs and eligibility. Production timing and partner selection must be recalculated according to IAA thresholds – choices between KD assembly and full local supply chains will directly affect subsidy eligibility and procurement competitiveness. EU countries with mature automotive industries, such as Spain and the Czech Republic, offer higher certainty in meeting “Made in EU” standards compared with Turkey; the strategic value of existing Turkish layouts should be reassessed.

- Seize opportunities in European component M&A: Europe’s traditional component sector is undergoing structural adjustments with abundant targets at reasonable valuations. As local industrial protection policies strengthen, this window is closing. For Chinese suppliers aiming to deepen the European market, now is the last opportunity to acquire local manufacturing capability and customer relationships through M&A.

- Incorporate policy uncertainty into investment decisions: The IAA is still a draft, and final provisions may change through trilateral negotiations. This is not a reason to “wait and see” – on the contrary, the draft phase is the lowest-cost window to adjust investment pace, lock in partners, and reassess market priorities. Enterprises should prepare scenario-based decision plans in advance; those capable of quickly switching execution paths once regulations are finalized will gain a significant first-mover advantage.

Our Services

In response to the rapidly evolving EU policy environment, we provide the following support to Chinese enterprises seeking to establish or deepen their presence in the European market:

- European Market Entry Strategy: Market assessment, GTM path planning, localization production timing, and partner selection.

- Compliance Assessment and Response: Evaluate compliance gaps and response paths for existing business under the IAA, FSR, anti-subsidy tax, and other policy frameworks.

- Equity Structure Design: In line with regulatory investment condition requirements, assist in planning foreign ownership ratios, joint venture structures, and entity establishment to ensure investment structures meet approval conditions while balancing commercial interests.

- Overseas Supply Chain Development: Supply chain restructuring, EU-origin compliance planning, and local procurement strategy design.

- Cross-Border M&A: Target screening in Europe, due diligence support, transaction structure design, and integration planning