Executive Summary

China’s outbound M&A is re-entering the market conversation, but under a discipline that looks structurally different from the last peak cycle. Disclosed outbound deal value rebounded in 2025 while deal count increased only modestly with an early-cycle profile that typically reflects selective re-activation driven by a smaller number of larger, financeable situations rather than broad-based risk appetite. In consumer, the deals that clear today’s constraints are increasingly those where structure can underwrite execution: staged risk, credible governance access, and a value-creation plan that is operationally specific.

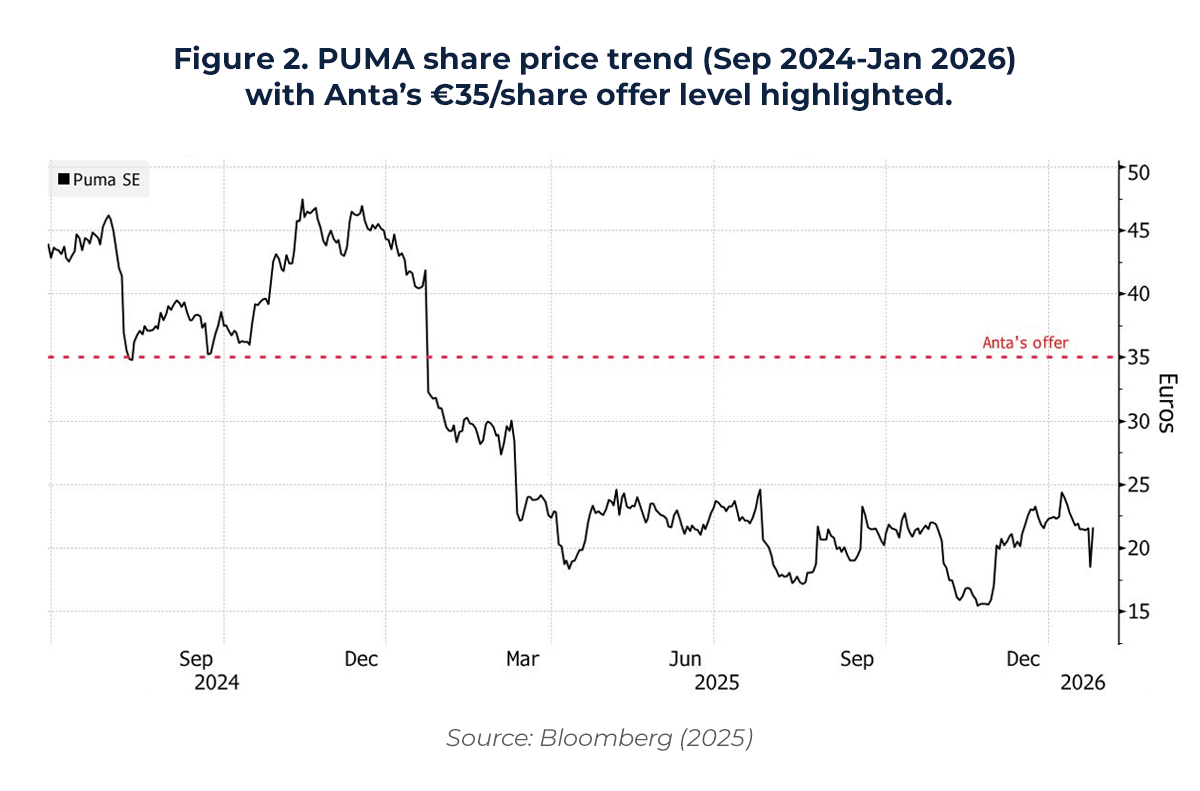

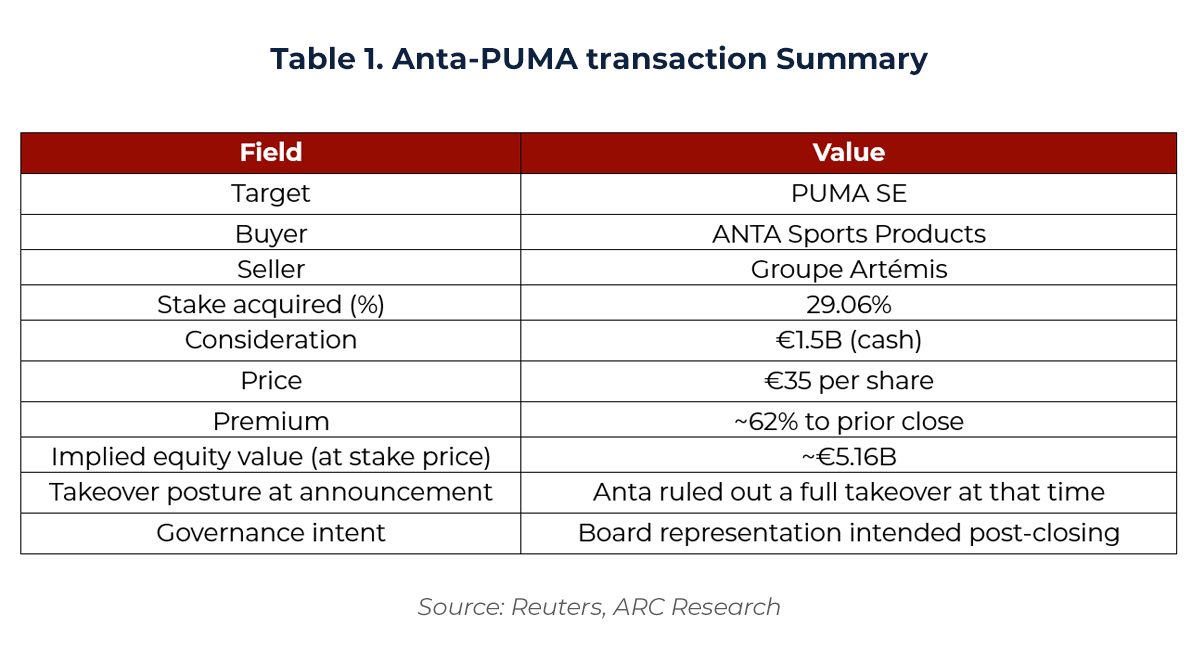

Anta’s move on PUMA captures that shift in one transaction. What initially surfaced as potential takeover interest resolved into a structured block-stake acquisition: Anta agreed to acquire 29.06% of PUMA from Groupe Artémis for €1.5B in cash, at a reported €35 per share level implying a substantial premium to the prior close. The stake size is commercially meaningful in Germany, where 30% voting rights is widely treated as a control threshold in the takeover framework. The result is an engineered entry that delivers strategic relevance and a pathway to influence without forcing an immediate control process or day-one integration.

The operating context strengthens the lens. PUMA entered 2025 in a reset phase by tightening distribution quality, reducing undesirable wholesale exposure, and leaning on DTC to protect revenue quality while absorbing near-term pressure from promotions and inventory clean-up. In this setup, the central question is not “synergies on paper,” but whether an anchor shareholder can support governance stability and execution cadence while the operating reset plays out. Importantly, minority-first structures also carry distinct risks: absent investable governance terms and message discipline, a near-control stake can create visibility without influence by fueling narrative volatility, blurring accountability, and triggering expectation-driven reactions across channels and talent that can dilute recovery.

Key Takeaways

- Outbound consumer M&A is becoming feasible again in selective cases, but the clearing set increasingly requires a fixable asset in transition and a clean scale entry mechanism (block or structured pathway).

- The Anta–PUMA structure illustrates minority-first entry engineered around a control threshold, with governance design as the determinant of whether ownership converts into influence or creates noise.

- Credibility is now earned through a localised, measurable operating thesis and early scoreboards via channel discipline, DTC economics, inventory/promotion control, and Asia/China trajectory rather than abstract synergy narratives.

I. Outbound in 2025: A Recovering Market with a Higher Burden of Proof

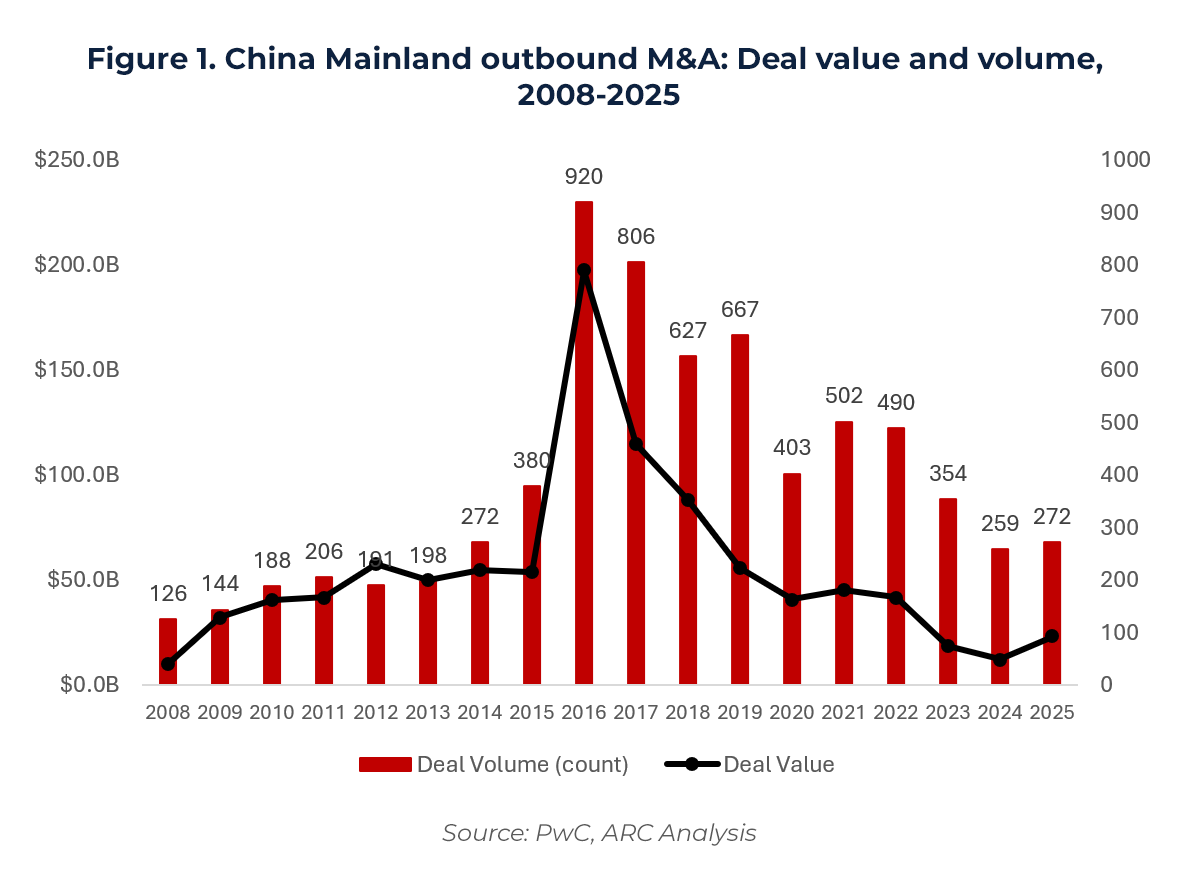

The post-2016 reset in outbound activity has been well understood for several years: policy, financing conditions, and risk appetite all tightened. What changed in 2025 is that outbound deal value visibly rebounded from a low base, while volumes remained modest.

The outbound market is no longer in the “structural shutdown” phase, but it is also not operating on the permissive assumptions of the prior peak cycle. The 2025 rebound from a low base matter, yet the bigger shift is behavioral: transaction design now carries more weight in underwriting than it did in the last cycle.

For corporate decision-makers, this distinction matters. A rising value line does not mean “go back to 2016.” It means cross-border is increasingly possible again, and buyers are increasingly incentivized to structure entry in a way that protects downside, particularly in consumer and branded assets where value can be destroyed quickly through governance instability, positioning ambiguity, or integration missteps.

II. Anta-PUMA: From “Exploring a Bid” to a Block Stake

II. Anta-PUMA: From “Exploring a Bid” to a Block Stake

The public narrative began with a familiar setup of a potential takeover: a globally recognized listed brand under pressure, a cornerstone shareholder with a clean block, and market talk of strategic interest. In late 2025, reporting indicated Anta was exploring a possible bid for PUMA and might partner with a private equity firm if it proceeded. That framing is a common because it signals the initial “control transaction” lens through which markets tend to interpret cross-border situations: a listed global brand appears strategically “in play,” especially when a large cornerstone shareholder is understood to be evaluating options.

What in fact occurred in January 2026 was structurally different and shifted that lens. Anta reached an agreement to acquire 29.06% of PUMA from Groupe Artémis for €1.5B in cash, with reporting pointing to €35/share pricing and a sizeable premium. Anta also stated it was not pursuing a full takeover at that time. The deal therefore resolved not as a control transaction, but as a strategic block acquisition. This is not merely “less ambitious” than a full bid but a deliberate sequencing choice. A stake of this size makes Anta the largest shareholder and creates a credible path to governance influence, while reducing the immediate need to integrate systems, leadership, or brand decision-making across borders.

The transaction sequence is precisely what makes the case instructive. It shows how modern outbound deals can shift from “headline takeover” speculation to a structure that is easier to finance, easier to execute, and easier to defend to stakeholders is more consistent with today’s outbound constraints:

1. Acquire a strategically meaningful stake.

2. Secure a pathway to governance influence.

3. Focus value creation on execution levels that are realistically transferable:

- distribution discipline

- retail productivity

- brand portfolio architecture

- market-specific acceleration (including China)

III. Deal Mechanics: Why 29.06% Is the Story, Not the Headline

The market’s first instinct is to read Anta–PUMA as “minority versus control.” That framing misses what is most instructive: the stake level and the entry route are engineered, and the structure is doing underwriting work consistent with how outbound consumer deals are increasingly executed in this cycle.

1) 29.06% is designed around the 30% control threshold

Anta’s 29.06% position is not “near 30%” by coincidence. In Germany, 30% of voting rights is widely treated as a control threshold in the takeover framework. Crossing that line can shift a shareholder into a different procedural and signalling regime, including heightened expectations around mandatory-offer mechanics and an eventual control outcome.

Staying below the line is valuable for three reasons:

- Optionality with intent. Anta can become the anchor shareholder and pursue governance engagement without committing to a near-term tender pathway. In a consumer asset still in reset, this is risk sequencing, not indecision.

- Lower narrative friction. A control trajectory can rapidly reshape stakeholder behaviour of employees, partners, and management regardless of what the buyer intends. Staying below 30% reduces the probability that the situation becomes dominated by “takeover mechanics” before the relationship is established.

- Influence with speed. In many listed-company contexts, formal control is not required on day one to be consequential. A near-30% stake can establish the buyer as the reference shareholder and provide a credible platform for governance access post-closing.

In short, 29.06% can deliver influence potential without forcing an immediate control posture as a feature, not a compromise, in today’s outbound environment.

2) The block purchase is one of the few clean ways to build scale quickly

In a listed European consumer asset, there are only three practical routes to build a meaningful position:

- gradual market accumulation (slow, visible, exposed to price drift),

- a full public offer (fast but escalatory),

- a negotiated block from a cornerstone holder (scale with certainty).

Anta chose the third route. A bilateral block delivers defined pricing, timing, and scale in one step by reducing the risk of ending up with meaningful exposure but an unclear pathway for engagement. It also avoids a common failure mode: the market interpreting a staged build-up as a prelude to control before the buyer has decided whether control is desirable.

For outbound buyers, this constraint matters. Strategic interest is common; clean entry points at scale are not.

3) Structure as sequencing: governance first, integration optional

This transaction is best understood as sequencing. In consumer brands, the highest-impact risks are often concentrated in the first 6–12 months through brand positioning stability, channel confidence, management focus, and operating cadence. A minority anchor stake can protect that phase by allowing the relationship to be judged on governance and execution rather than on takeover speculation.

The logic is straightforward:

- establish relevance as the reference shareholder;

- institutionalise governance engagement in a listed-company setting;

- let the operating trajectory validate (or reject) any future escalation.

That sequencing keeps the “end state” from dominating the narrative and allows the next step to be earned rather than presumed.

4) What the deal mechanics tell us about the current outbound market

The key takeaway is not that Chinese strategics suddenly discovered overseas consumer assets but they have long been interested. The takeaway is that feasibility is increasingly engineered through stake design and entry structure. In a market reopening selectively, transactions are more likely to clear when buyers can shape the execution profile up front: a clean block, a deliberate stake level, and a credible governance pathway that avoids unnecessary control mechanics.

IV. Operating Context: What the Market Can Observe

For a listed consumer brand, the most useful scoreboards tend to sit in (i) channel mix and revenue quality, and (ii) regional trajectory, particularly where the business has been underperforming.

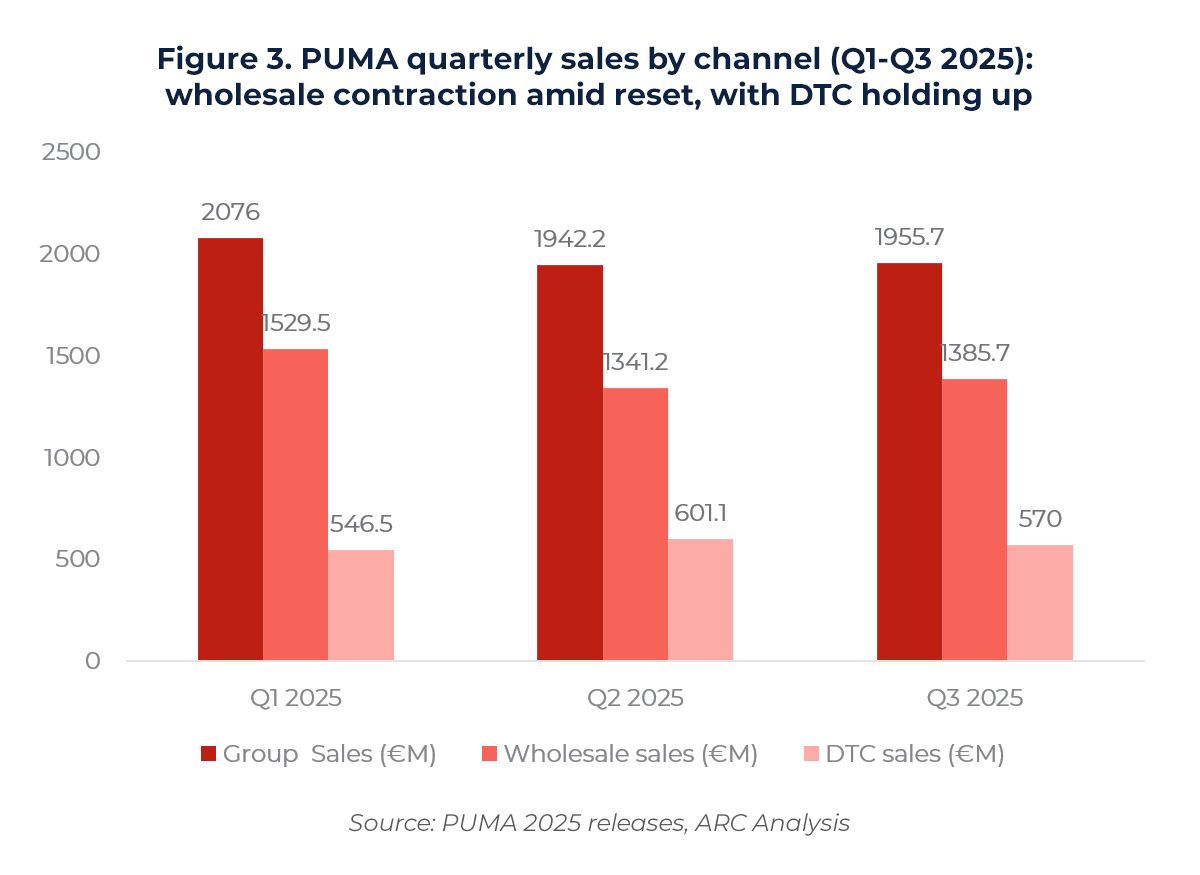

1) Channel mix: DTC resilience versus wholesale pressure

PUMA’s reported channel split through 2025 provides a clean, mechanical baseline. In Q1-Q3 2025, DTC represented a higher share of group sales than in early 2025, while wholesale remained at the larger base but showed pressure in absolute terms. This mix matters because it affects both margin quality and brand control: DTC typically gives the brand more control over pricing, inventory, and consumer experience, while wholesale scale can amplify growth but also amplifies volatility when the channel is stressed.

The commercial reality is that the brand is not being acquired at the top of a growth cycle but it is being underwritten at a moment where execution discipline becomes the primary determinant of recovery.

This operating context reframes the acquisition logic. A sophisticated buyer is not paying for near-term acceleration, but it is underwriting the recovery profile and the quality of earnings that can emerge after distribution quality improves. In consumer deals, that is often where long-term value hides – inside unglamorous mechanics like channel discipline, inventory normalization, and retail productivity.

Where does a strategic shareholder potentially matter? Not by “integrating” PUMA into Anta, but by reinforcing a scoreboard and cadence that supports the reset:

- protecting distribution clean-up from short-term volume temptation,

- improving channel economics through DTC/wholesale calibration,

- and accelerating market execution where a credible operator has an advantage (China is the obvious candidate, but it must be treated as KPI-driven, not narrative-driven).

2) China: why it is an opportunity and a constraint

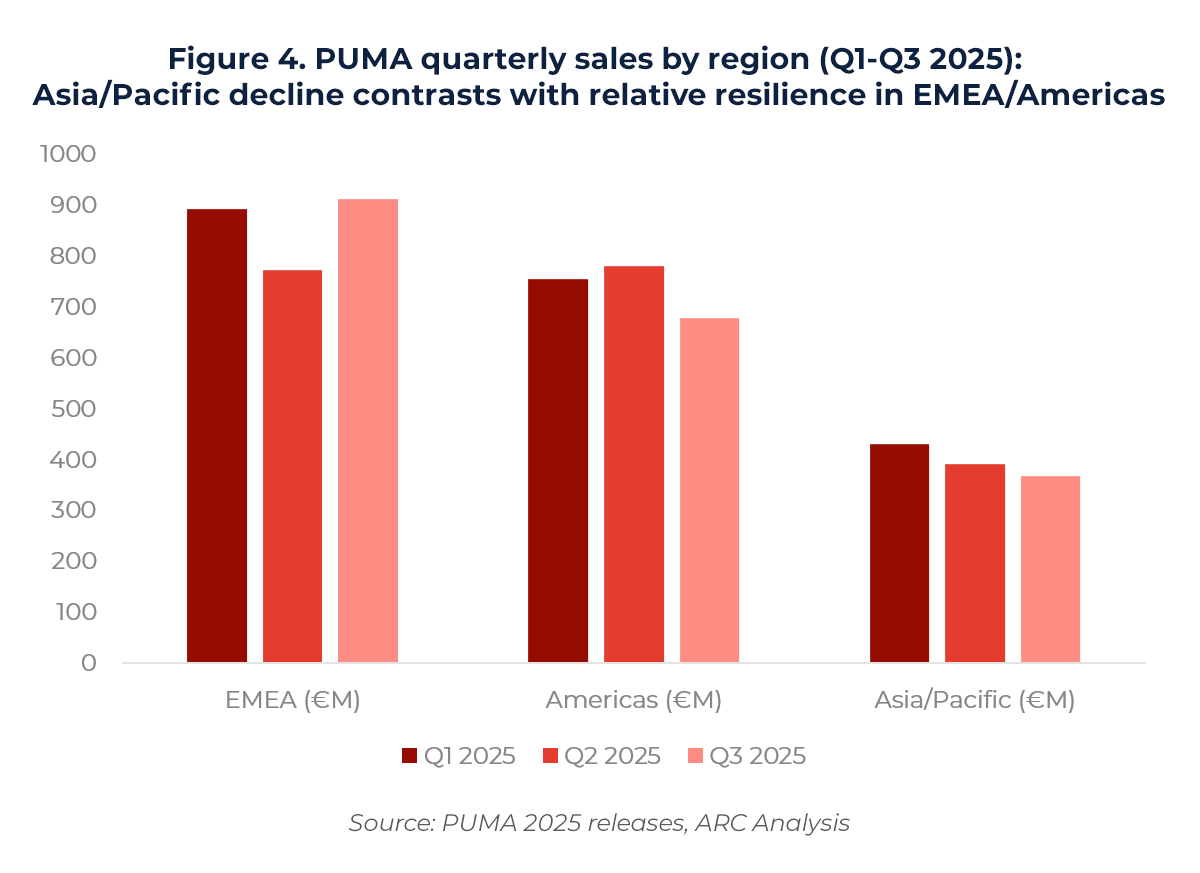

Regional performance provides the second baseline. Across Q1-Q3 2025, PUMA’s reported sales show Asia/Pacific declining sequentially, while EMEA and the Americas fluctuate but appear comparatively more stable over the same period. This is not a “China conclusion” by itself, but it defines the starting point for any narrative that assumes upside in Asia/China.

The important nuance is that PUMA also linked parts of its Asia/Pacific weakness to executed reset actions (including wholesale adjustments), while DTC grew. That tells us two things simultaneously:

- China is not a blank canvas where execution alone guarantees upside. It is a market where the brand is already navigating channel quality and demand softness.

- At the same time, China is one of the few markets where an operator’s cadence (partner selection, inventory discipline, retail productivity systems) can create meaningful outcome differences without changing the global brand identity.

In practical terms, the earliest evidence of value capture is unlikely to be headline growth. It will show up first as stabilization in Asia/Pacific trajectory alongside sustained DTC strength and improving channel health.

V. Signals for China outbound consumer M&A

The Anta-PUMA structure is best understood as part of a broader pattern: outbound transactions that are viable today tend to be those where the buyer can credibly demonstrate operating relevance without demanding immediate control. For consumer assets, the transaction form increasingly reflects three conditions:

- the asset is in a reset or at least in a transition phase,

- a clean block exists (or a structured pathway can be negotiated),

- the buyer’s value creation is rooted in measurable operating levers rather than conglomerate integration.

This is not a statement that “minority stakes are always better.” It is a statement that the constraint set in 2025-2026 makes risk sequencing a first-order decision variable.

1) The best outbound consumer targets will look “fixable,” not “perfect”

Today’s viable opportunities tend to share a common setup: the asset is already in a transition (channel clean-up, inventory correction, brand repositioning), and there is a credible mechanism to enter at scale (a cornerstone seller, a negotiated pathway, or a pre-arranged governance package). Buyers are not paying for peak-cycle growth; they are underwriting a recovery where execution discipline is the value.

Signal: expect more outbound activity where the seller side can deliver a clean block and where the asset is in a reset that can be measured quarter-by-quarter.

2) The operating thesis must be explicit and localised

Markets are less tolerant of “global synergy” narratives in consumer assets. The value creation case needs to be stated in operational terms: what changes in distribution, retail productivity, product architecture, and China/Asia execution and who owns those levers, and what early KPIs would confirm progress.

Signal: buyers will be judged on whether they can point to transferable operating playbooks (e.g., China acceleration systems) rather than “group integration.”

3) Governance design is becoming central to outbound success.

Minority positions only work if governance terms translate ownership into influence without destabilising management. That means clarity on board representation, information rights, and boundaries: strategic direction and performance cadence can be influenced, while brand identity and day-to-day operations remain coherent.

Signal: governance packages (board, committees, information cadence, standstill/intent language) will increasingly be disclosed or at least understood as essential because they determine whether “minority” is meaningful.

Bottom line: the Anta–PUMA structure reflects a market where the question is no longer “control or not,” but “how to underwrite execution without importing unnecessary process risk.” That is why transaction design is now part of the investment case in outbound consumer M&A.

VI. Risks: Where This Deal Form Can Create Value or Create Noise

A near-control stake can preserve operational stability versus an immediate takeover, but it introduces a different risk profile. In listed consumer brands, the early success or failure of “minority-first” structures is often determined less by synergy plans than by governance clarity and message discipline. When the asset is already in reset, small signals are amplified: stakeholders do not wait for an end state to form a view.

1) Governance ambiguity: influence is assumed, but not guaranteed

A 29% anchor position inevitably changes market expectations. Even if the buyer has no immediate control intent, investors, employees, distributors, and counterparties will price in the possibility of strategic redirection. If the governance framework is not clearly defined by terms that explain who sits where, how strategic input is provided, what information cadence exists, what decisions remain fully management-led then the stake can create visibility without effective influence.

That gap produces two types of noise:

- Narrative volatility: repeated speculation about “what Anta wants” can overwhelm the operating reset story, particularly if communications are inconsistent or overly cautious.

- Accountability blur: when performance improves, it is unclear whether it reflects management execution or shareholder intervention; when performance deteriorates, it becomes easier for each side to signal “not us.” That ambiguity can weaken confidence exactly when credibility is most valuable.

This is why, in practice, minority anchor stakes work best when engagement is institutionalised (board/committee representation where appropriate, structured interaction routines, and a stable public posture) and when boundaries are explicit (strategic guidance vs day-to-day autonomy).

2) Stakeholder signalling risk: the structure can trigger second-order reactions

Consumer brands are unusually sensitive to expectations. Channel partners, athletes/agents, suppliers, and key hires respond to perceived shifts in ownership intent long before any operational change is implemented. A near-control stake can therefore create self-reinforcing dynamics:

- wholesale partners may become more conservative on forward orders if they anticipate pricing or distribution changes;

- promotional behaviour can intensify if counterparties expect inventory clearing or channel rebalancing;

- talent decisions can be delayed if teams are uncertain about future leadership direction.

These are not “integration risks” in the classic sense but they are expectation risks, and they can erode the very stability that minority-first structures are meant to protect.

3) China execution risk

China is not “plug-and-play.” The operational opportunity is real, but it is bounded by brand positioning, consumer perception, competitive intensity, and the constraints of a global brand identity that cannot be localized beyond recognition. Success requires disciplined retail execution and brand stewardship, not simply more stores or more discounting.

4) Operating-cadence mismatch: strategic urgency vs brand reset timing

A strategic shareholder typically arrives with an execution playbook and a desire for measurable progress. A brand in reset often requires the opposite: sequencing, consistency, and careful pacing in channel discipline, product architecture, and marketing. If cadence expectations diverge then even rational initiatives can look like churn. In public markets, churn gets penalised.

The risk is not that a shareholder pushes for “synergies,” but that governance dynamics unintentionally accelerate decision cycles, increasing organisational noise and weakening the coherence of the reset.

5) Market-wide implication: minority-first structures raise the premium on governance design

At the market level, Anta–PUMA highlights a broader constraint for China outbound consumer M&A: as control transactions become harder to underwrite and execute cleanly, governance becomes the deal. The risk is that more cross-border stakes are announced without sufficiently credible governance arrangements while creating headline activity but limited operational traction. Over time, that can:

- increase scepticism toward outbound “strategic minority” announcements;

- compress valuation uplift from such deals;

- make sellers and boards more cautious unless governance terms are clearly investable.

Bottom line: a near-control stake can be a low-disruption way to enter a global consumer platform but only if governance is sufficiently explicit to convert ownership into stable influence. When it is not, the structure can generate uncertainty that overwhelms execution, and the market will treat the stake as noise rather than a value-creation instrument.

VII. Strategic Message

1) What stakeholders are signalling

This deal communicates different messages to different investor bases, and the structure is what makes those messages coherent.

- Anta shareholders: a controlled entry into a global platform. The underwriting is governance access and an executable operating thesis and not immediate consolidation.

- PUMA shareholders: a reference shareholder during a reset. The upside is longer-term stability and execution discipline; the risk is added noise if governance intent and boundaries are not clear.

- Artémis (seller): a clean liquidity event for a large block. The transaction reinforces that structured block exits remain feasible in listed European consumer assets when the buyer can underwrite optics, governance, and process constraints.

2) What the market should take from this case

This deal communicates a set of market-wide signals that extend beyond Anta and PUMA:

- Structure is now part of the investment case. Engineered entry is replacing “transformational takeovers” as the more executable path in outbound consumer deals.

- Governance is the deal. Minority-first stakes only create value if terms translate ownership into stable influence; otherwise they invite narrative volatility and discounted outcomes.

- Execution must be measurable and localised. Credibility increasingly comes from specific operating levers and early scoreboards via channel discipline, inventory/promotion control, and Asia/China cadence rather than abstract synergy language.

Bottom line: Anta–PUMA signals a cycle where outbound consumer M&A is reopening selectively, but outcomes will be determined by whether buyers can combine a fixable asset, a clean entry mechanism, and investable governance that reduces noise while enabling execution.

Conclusion

Anta’s move on PUMA fits the current logic of China’s outbound consumer market: the recovery in activity is real, but it is increasingly expressed through structures that prioritise sequencing, governance access, and controlled execution risk rather than immediate control. A near-30% block stake can deliver strategic relevance and a pathway to influence without forcing a takeover posture or day-one integration with an approach that is becoming more workable under today’s regulatory, stakeholder, and operating constraints.

At the same time, the case underscores why “minority-first” is not automatically benign. In a listed brand undergoing a reset, an anchor stake can just as easily create noise if governance is not sufficiently explicit to translate ownership into stable influence. Ambiguity around engagement mechanisms and boundaries can fuel narrative volatility, blur accountability, and trigger expectation-driven reactions across channels and talent dynamics that can dilute recovery even when the operating plan is sound. The implication for the broader market is clear: the next phase of Chinese overseas consumer M&A is likely to be defined by engineered entry into “fixable” assets with credible scale pathways, but outcomes will increasingly be determined by whether governance is investable and whether the buyer can articulate a localised operating thesis, clear early KPIs, and disciplined pacing.

About ARC Group

ARC advises Chinese companies on cross-border M&A and strategic transactions, with a focus on situations where value creation depends on execution, governance design, and operational relevance not headline control. We support clients across the full transaction lifecycle, including deal strategy and positioning, target screening and buyer/partner mapping, valuation and deal modeling, diligence workstreams, negotiation support, and cross-border execution management.

In consumer and industrial sectors, ARC’s work frequently centers on complex “engineered entry” structures including minority anchors, staged pathways, carve-outs, and partnership-capable frameworks where stakeholder optics, regulatory thresholds, and operating cadence can determine outcomes as much as price. Leveraging our regional network across China, Europe, and Southeast Asia, ARC helps management teams and shareholders identify executable pathways, reduce process and integration noise, and translate strategic intent into measurable operating results.

The financial figures and transaction details presented in this article are derived from publicly available sources, including press releases and media reports. As such, they are intended for illustrative and educational purposes only and may not fully reflect the actual deal structure, terms, or confidential elements of the transaction. Readers should not rely solely on this information for investment, legal, or financial decision-making.

References:

- PwC. (2026) “China M&A 2025 Review and Outlook”

- Bloomberg (2024–2026). PUMA equity price history; event window for stake announcement.

- Anta Sports Products Ltd. (2026). Company announcement / HKEX filing related to acquisition of PUMA stake (primary disclosure)

- PUMA SE (2025). Q1-Q3 2025 Quarterly release / interim statement (IR).

- PUMA. (2018) Corporate communication on ownership structure change and planned distribution of PUMA shares

- Reuters. (2025) “China’s Anta Sports exploring bid for Puma, Bloomberg News reports”

- Reuters. (2026) “China’s Anta Sports buys 29% Puma stake for €1.5 billion, rules out full takeover”

- BaFin (Federal Financial Supervisory Authority, Germany). Takeover law overview / control threshold and mandatory offer framework (WpUG)

- German Securities Acquisition and Takeover Act (WpÜG). Statutory text and definition of control / mandatory offer triggers.

- Kering (2018). Project to distribute in kind PUMA shares to Kering shareholders (distribution announcement / documentation).