Companies pursuing a U.S. listing, whether through an IPO, direct listing, or alternative pathways such as SPAC mergers or reverse takeovers, face one constant strategic variable: timing. While valuation, business fundamentals, and investor readiness remain central, the market window ultimately determines whether a listing achieves its objectives or stalls. Understanding how timing interacts with liquidity conditions, sector sentiment, macroeconomic catalysts, and regulatory dynamics is essential for issuers and stakeholders preparing to enter U.S. public markets. In practice, timing determines not just when a company lists, but whether it lists at scale, at valuation, and with durable investor support.

Market, Economic, and Regulatory Factors

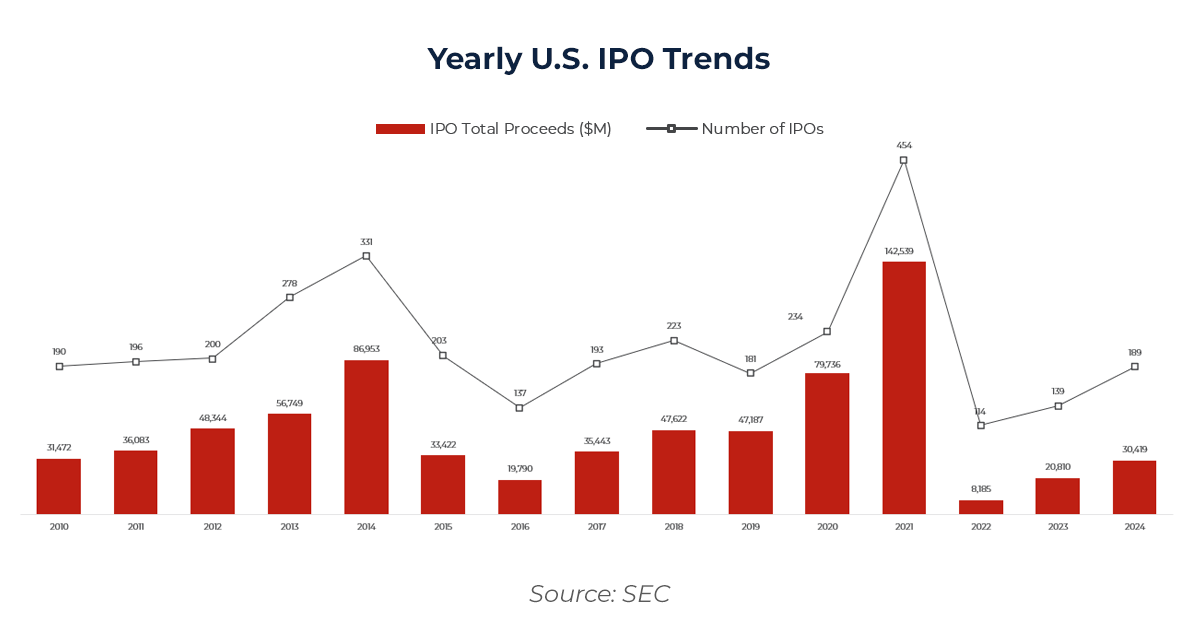

Market windows have historically opened and closed in cycles tied to investor risk appetite, broader market and macroeconomic conditions. Deal volumes tend to cluster around periods of strong equity performance, stable interest rates, and lower volatility. Historical issuance cycles consistently show that IPO activity clusters around periods of stable rates, expanding liquidity, and positive equity momentum. Conversely, periods of rising rates, election uncertainty, or geopolitical stress consistently depress issuance as investors become more selective and price sensitive.

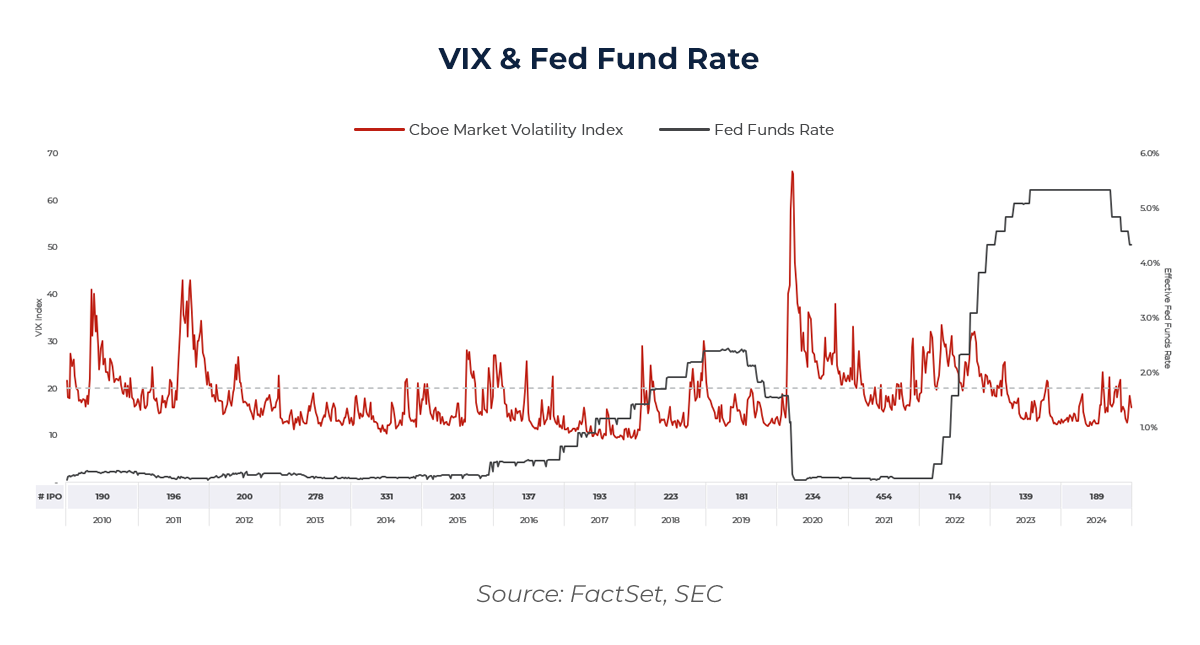

One of the most powerful indicators of market readiness is market volatility. The Cboe Volatility Index (VIX) often serves as a proxy for investor sentiment, and U.S. IPOs tend to pull back when volatility remains high for an extended time (usually when VIX is above 20). High volatility constrains institutional investors’ ability to underwrite risk, compresses valuation multiples, and elevates the likelihood of IPO withdrawals or downward pricing revisions. Listing data from prior strong issuance cycles confirms that most successful IPOs price when volatility stabilizes and forward equity returns turn positive. Issuers sensitive to valuation often adjust their timelines to avoid windows where volatility threatens capital formation.

One of the most powerful indicators of market readiness is market volatility. The Cboe Volatility Index (VIX) often serves as a proxy for investor sentiment, and U.S. IPOs tend to pull back when volatility remains high for an extended time (usually when VIX is above 20). High volatility constrains institutional investors’ ability to underwrite risk, compresses valuation multiples, and elevates the likelihood of IPO withdrawals or downward pricing revisions. Listing data from prior strong issuance cycles confirms that most successful IPOs price when volatility stabilizes and forward equity returns turn positive. Issuers sensitive to valuation often adjust their timelines to avoid windows where volatility threatens capital formation.

Interest rate expectations play an equally important role. While higher rates do not directly preclude listings, they materially influence equity risk premium, discount rates, and sector rotation. Federal Reserve guidance, especially through FOMC projections, economic policy statements, and inflation trends, shapes investor appetite for growth-oriented issuers. Periods of expected rate stability or cuts typically align with stronger IPO performance, as seen in early 2024 when renewed confidence in disinflation supported a rebound in U.S. issuance. Conversely, when real rates rise, public-market investors disproportionately favor value and cash-generative sectors, narrowing the window for earlier-stage technology or biotech issuers. As a result, issuers often accelerate or defer filings not based on absolute rate levels, but on whether the direction of policy feels predictable to investors.

Interest rate expectations play an equally important role. While higher rates do not directly preclude listings, they materially influence equity risk premium, discount rates, and sector rotation. Federal Reserve guidance, especially through FOMC projections, economic policy statements, and inflation trends, shapes investor appetite for growth-oriented issuers. Periods of expected rate stability or cuts typically align with stronger IPO performance, as seen in early 2024 when renewed confidence in disinflation supported a rebound in U.S. issuance. Conversely, when real rates rise, public-market investors disproportionately favor value and cash-generative sectors, narrowing the window for earlier-stage technology or biotech issuers. As a result, issuers often accelerate or defer filings not based on absolute rate levels, but on whether the direction of policy feels predictable to investors.

Sector sentiment plays a pivotal role in defining sub-cycles within the broader IPO market. For example, the 2020–2021 period was characterized by a surge in software-as-a-service (SaaS), and biotech listings, driven by strong thematic investor flows and significant retail participation. During the 2024 cycle healthcare and TMT (technology, media, and telecom) were the leading sectors of investor interest. Companies that do not align with current technological advancements or investor preferences often face larger valuation discounts or reduced demand, even when broader market indicators are positive.

Liquidity conditions, both institutional and retail, also dictate window strength. Institutional liquidity is influenced by fund flows, positioning, and quarterly performance cycles. Public funds tend to commit capital more actively in the first half of each quarter, following portfolio rebalancing and before earnings periods. In contrast, the fourth quarter often sees reduced issuance due to year-end constraints and holiday-driven liquidity declines. Retail liquidity, while smaller in absolute terms, has become more relevant due to zero-commission trading environments and social-media-driven attention cycles. Retail flows can support short-term liquidity, but institutional positioning remains the primary determinant of window strength.

Regulatory and disclosure readiness are additional factors that shape timing choices. The SEC review process for S-1 or F-1 filings introduces inherent unpredictability, often requiring issuers to build in additional flexibility when targeting a market window. During periods of high filing volume, review cycles may extend, affecting the ability to coincide with optimal issuance windows. In recent years, expansions in disclosure expectations have increased execution complexity, particularly for cross-border issuers. Issuers that enter the filing process unprepared typically miss attractive windows when market conditions shift more quickly than expected.

The Trade-Off Between Speed and Valuation

The trade-off between speed and valuation is at the center of every timing decision. Strong market windows typically allow issuers to optimize valuation and size while securing high-quality institutional support. Weaker windows may still permit listings but often at the expense of pricing, dilution, or reduced capital proceeds. Many issuers choose to postpone during softer periods, especially if their funding needs are not immediate. However, waiting too long introduces its own risks. Competitive dynamics, operational underperformance, or macro deterioration can erode valuation significantly than a moderate pricing discount would have. Striking the right balance requires a data-driven assessment of momentum indicators, sector capital flows, and internal readiness. Experienced issuers treat timing as a risk management decision, not a market-timing exercise.

Historical data illustrates the magnitude of this trade-off. During the 2021 peak window, U.S. IPOs priced at an average first-day pop of 31% and routinely achieved oversubscribed books. By contrast, in the 2022–2023 downturn, many issuers that insisted on peak valuations from earlier years either withdrew or priced significantly below range. The eventual 2024 reopening demonstrated that well-prepared companies could achieve strong outcomes by aligning their offering with a clear recovery in market sentiment and institutional risk appetite. Timing discipline, not simply waiting for ideal conditions, was the differentiating factor.

For cross-border companies, timing considerations additionally reflect currency trends, local regulatory reforms, and investor appetite for international exposure. Strengthening of the U.S. dollar generally supports foreign issuers by reducing translation losses and increasing the relative attractiveness of U.S. capital markets. Conversely, periods of geopolitical tension can amplify due diligence and regulatory scrutiny, prolonging time-to-market. Issuers with internationally diversified revenue bases and strong governance frameworks tend to perform better in these windows.

Conclusion

In conclusion, the timing of a U.S. listing is a complex yet critical factor for issuers seeking to achieve their desired outcomes. A deep understanding of market conditions, sector sentiment, regulatory readiness, and liquidity factors is essential to navigating this process successfully. Issuers must balance the trade-off between seizing an optimal market window and ensuring that their valuations, business fundamentals, and investor readiness align with the broader macroeconomic environment. At ARC Group, as a trusted financial advisor, we play a pivotal role in helping clients assess these dynamic factors, offering data-driven insights and strategic counsel to ensure that they not only enter the market at the right time but also position themselves to maximize valuation and investor demand. Our expertise in managing market timing, coupled with our comprehensive understanding of regulatory requirements and sector-specific trends, enables us to guide clients through the complexities of U.S. listings, ensuring their success in the public markets.

Author:

Patrik Kohary

Capital Markets Analyst

References: