Executive Summary:

Despite a volatile macroeconomic backdrop and a more selective global capital market, restructuring activity across the DACH industrial sector is accelerating. ARC’s conversations with industrial corporates, strategic investors, and financial sponsors active across Europe point to a clear shift in transaction dynamics: portfolio reshaping is increasingly being executed through carve-outs, minority investments, and structured partnerships rather than full platform acquisitions.

This development reflects a convergence of pressures on the region’s industrial base. Elevated energy costs, supply-chain realignment, technology disruption, and capital intensity associated with decarbonisation and digitalisation are forcing faster and more explicit capital allocation decisions. At the same time, traditional ownership models — long-term family control, conservative balance sheets, and reliance on domestic bank financing — are under strain.

As a result, high-quality industrial assets are becoming accessible through non-traditional ownership pathways, including minority stakes, continuity-driven restructurings, and corporate carve-outs. For foreign strategic investors and long-term capital providers, 2026 may mark an inflection point to participate selectively and constructively in the next phase of DACH industrial transformation.

This insight piece is the first in a series examining how structural shifts across DACH are reshaping deal structures, investor access points, and ownership outcomes. In Part II of this series, we will move from macro observation to deal execution: “DACH + Adjacent Europe Industrial Corridor: What to Buy and What to Sell?”

I. Overview of the DACH Industrial Sector

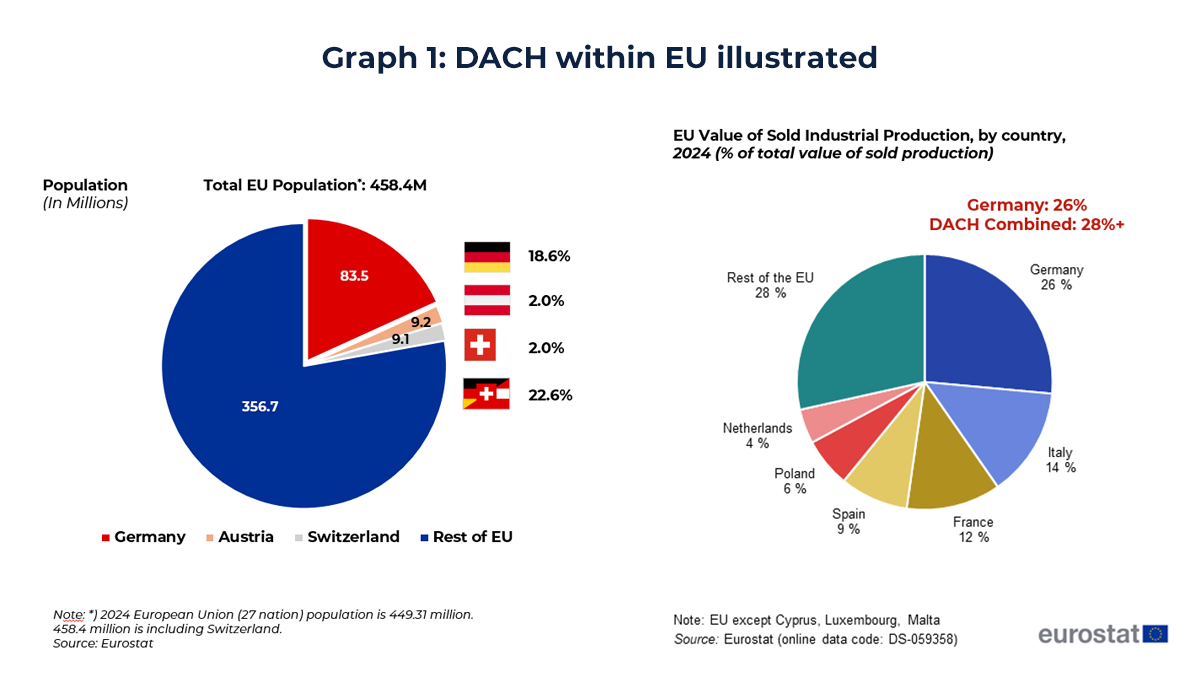

The DACH region – Germany, Austria and Switzerland – sits at the heart of Europe and has long formed one of the continent’s principal industrial cores, shaped by centuries of engineering, trade and manufacturing tradition. From the medieval guilds and early modern mining operations of the Alps to the rapid industrialization of the “Ruhrgebiet” (Ruhr Valley) and the Swiss watchmaking clusters, the region developed a distinctive economic model built on technical craftsmanship, incremental innovation and export discipline. This historical foundation laid the groundwork for DACH’s centrality to European manufacturing today.

With a combined GDP of around EUR 5–6 trillion and roughly 100 million inhabitants, the region represents one of Europe’s largest and wealthiest economic area. Its central location on Europe’s main rail and river corridors – linking North Sea ports with Italy, France and Central/Eastern Europe – and its dense network of inland logistics hubs make DACH a natural crossroads for European freight. Germany alone accounts for approximately 26% of European Union’s manufacturing output, while Switzerland ranks among the world’s most competitive economies driven by high innovation capacity, advanced industrial clusters, and an exceptionally skilled workforce.

A long‑standing “Mittelstand” (family-owned SMEs) culture of export‑oriented, often family‑owned manufacturers kept the region’s manufacturing share of GDP structurally higher than in most other advanced economies. Unlike the Anglo-Saxon model of frequent ownership changes and quarterly earnings pressure, DACH industrial companies have traditionally operated with longer investment horizons, substantial retained earnings, and close relationships with regional banks and skilled labor pools. This patient capital approach enabled sustained investment in automation, apprenticeship systems, and niche market leadership across sectors ranging from automotive components and machine tools to pharmaceuticals and industrial automation.

Yet this model now faces its most consequential test in decades. The post-2022 energy shock, the structural reorientation of global supply chains, rising competition from Asian manufacturers, and the capital requirements of transitioning to lower-carbon production have converged to challenge the economic fundamentals that sustained DACH industrial competitiveness for decades. Manufacturing energy costs in Germany, once a competitive advantage, spiked to multiples of those in the United States and parts of Asia. Geopolitical fragmentation has disrupted the export-led model which underpinned DACH industry’s global integration. Simultaneously, the automotive and machinery sectors that anchor the region’s industrial base confront technological disruption in electrification, digitalization and artificial intelligence that requires capital reallocation at unprecedented speed and scale.

These pressures are reshaping corporate strategy across DACH. Where organic growth and incremental expansion once sufficed, industrial companies now confront decisions about portfolio focus, capital efficiency, and ownership structures that many have deferred for years. It is within this context that carve-outs, minority stake transactions, and other forms of corporate restructuring have returned to the fore in 2026, representing a strategic response to structural change in Europe’s industrial heartland.

II. Key Trends of DACH Industrial Base: Strength Under Pressure

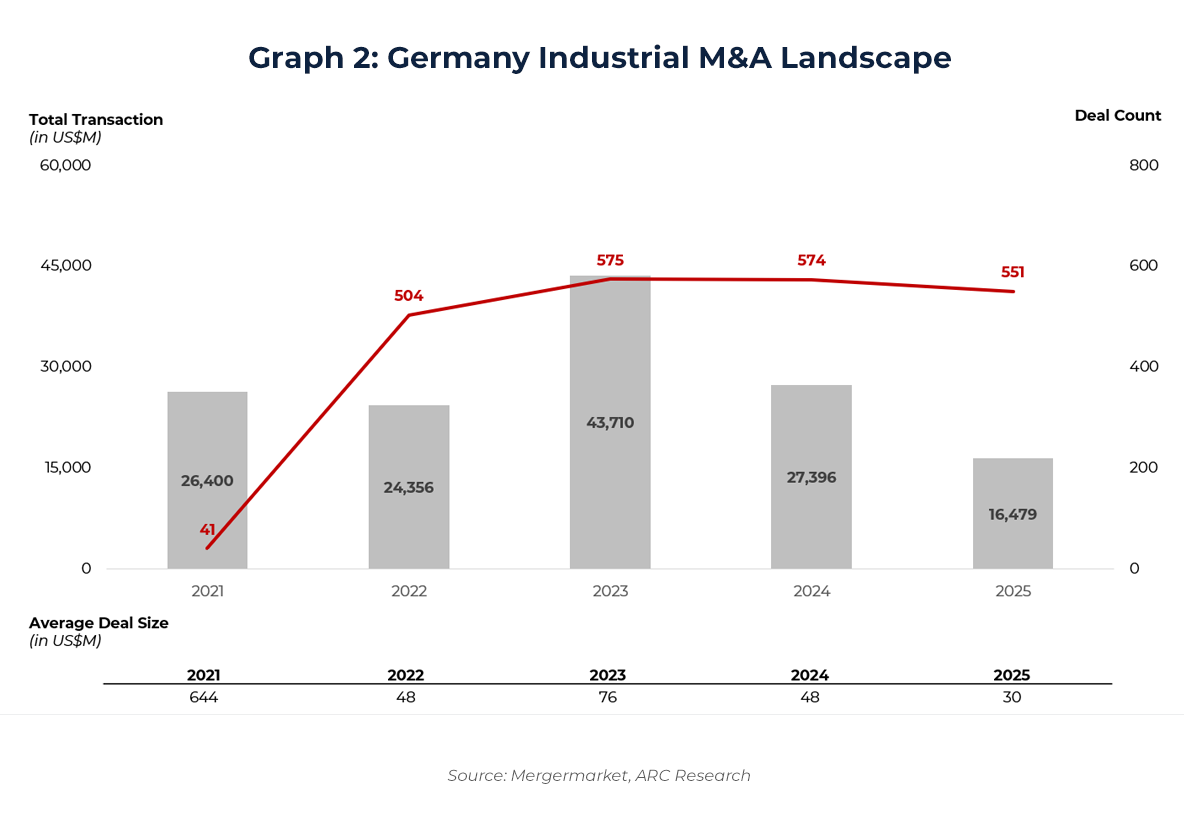

DACH industrial M&A activity softened through 2023–2024 amid elevated financing costs, energy shocks and supply chain fragmentation, but 2025–2026 deal flow has pivoted toward carve-outs, minority stakes and restructurings as corporates refocus portfolios for electrification, digitalisation and cost competitiveness. Industrial deal volume in Germany reached 551 transactions in 2025 – up 9.3% from 2022, though down from the peak in 2023. Total deal value moderated to EUR 16.5B, a 40% decline from the previous year, with average deal size decreasing to EUR 30M, reflecting a shift toward smaller transactions.

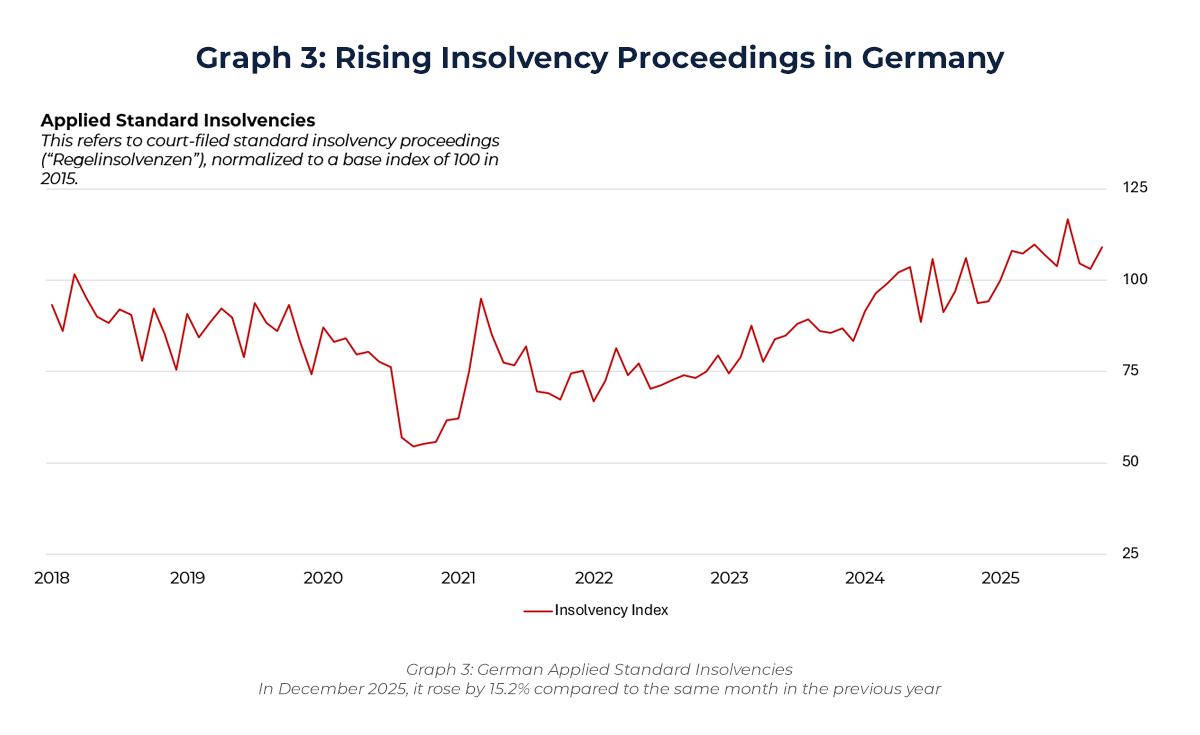

German insolvencies in manufacturing – particularly auto suppliers and machinery (Diepersdorf Plastic Manufacturing, Kiekert, AE Group etc.) – rose structurally in 2024–2025, creating a pipeline of distressed mid-caps where ownership redistribution via carve-outs or strategic sales preserves industrial capacity rather than liquidating it.

Giants like BASF and Volkswagen retain dry powder for selective consolidation, even as German firms broadly ramp outbound investments to China (EUR 7B in 2025, +55% vs 2023–24 averages), but inbound Asian flows—such as Chinese manufacturing takeovers—signal a two-way reshuffle where DACH assets gain new operators. Media narratives have shifted from recession fears to identifying “industrielle Langfristinvestoren“ (long-term industrial investors) as the real gap, positioning capable foreign strategics – including Chinese firms – as viable successors if they commit to operations, teams and customers.

- Carve-Outs from Legacy Portfolios

Rising energy costs and EV transitions have unbundled DACH conglomerates, with carve-outs targeting units in chemicals, components and machinery that lack standalone viability under public scrutiny or family ownership constraints. Sellers retain supply ties and minority interests, while buyers can access brands, IP and OEM relationships without conglomerate baggage; multiples hover at 5–10x EBITDA for mid-cap carve-outs, vs 10–13x for core assets. German bankruptcy processes now open these as continuity plays, isolating liabilities while teeing up operational handovers.

- Minority Stakes and Structured Partnerships Back in Favour

German companies remain fundamentally open to foreign minority stakes, viewing them as fresh equity capital and expertise for digitalisation and energy transition—without ceding control.

Mittelstand urgency stems from twin pressures: Pandemic-era KfW state loans (“Kreditanstalt für Wiederaufbau”) are maturing just as high energy costs have drained cash reserves, while weak automotive demand (EV sales stalled post-subsidy, China exports down) and machinery order slowdowns squeeze earnings. Meanwhile, structural shifts like German firms localising production in China permanently redirect investment away from domestic sites

The Federation of German Industries (BDI) highlights economic role of foreign ownership: firms drive over 20% of turnover and 10% of jobs. Strategic investors add long-term operational value through consensus governance; structures typically include call/put options tied to earnings multiples, drag-along/tag-along rights, and Mittelstand protections.

For DACH industrials in 2026, 10–30% stakes fund automation and renewables capex are ideal when they strengthen firms without compromising security. A pragmatic solution for equity-strapped mid-caps facing simultaneous cyclical and structural headwinds.

Marcus Stein (Deutsche Bank, Head Corporate Finance):

“… Dann sollten wir Lösungen sehen, die näher am Eigenkapital sind. Meine Erwartung wäre, dass wir in dem Zusammenhang auch zunehmend Diskussionen über Minderheitsbeteiligungen sehen werden.”

(We’ll see solutions closer to equity, and expect growing discussions around minority stakes.)

- Distressed Supplier Successors

When scale suppliers like Leoni enter restructuring, German discourse favors industrial operators over asset strippers. Leoni—a leading automotive wiring provider—faced 2023 pre-insolvency restructuring proceedings after EUR 1.6B debt overload from failed cable division sale and energy crisis—not demand collapse. The Germa media distinguished risky asset splits from industrial continuity plays; Pierer Konzern recapitalised Leoni in 2023, followed by Luxshare’s 2024 50.1% takeover (EUR 205M) of its Electrical Systems division—both prioritizing operational continuity over liquidation. Germany’s restructuring regime enables such handovers when restructuring valuation proves better creditor recovery than insolvency, creating structured entry points for manufacturing strategics committing to customers, engineers, and production networks. Luxshare’s deal validates Asian manufacturing as natural successors—Chinese industrials can navigate German restructuring by prioritizing business continuity over extraction.

Klaus Rinnerberger (CEO Leoni):

“Die einzige Alternative wäre Insolvenz gewesen. Kooperation mit Luxshare mildert Geschäftsmodellschwächen… Ich würde vielen Kollegen in der Zulieferindustrie schlichtweg raten, den Weg einer Kooperation zu suchen, anstatt gegen China ankämpfen zu wollen.”

(Insolvency was the only alternative. Luxshare cooperation mitigates business model weaknesses… I would simply advise supplier industry colleagues to seek cooperation rather than fight China.)

Such DACH companies lack capital but crave long-term industrial operators respecting its business logic. The 2026 pipeline offers foreign strategics prime access to distressed suppliers and carve-outs if they prioritise operational continuity over extraction, as Leoni’s Luxshare handover proves.

III. Deep Dive Case Studies (2023–2025)

Case Study 1: China’s Anta Sports snares 29% Puma stake for USD$1.5B

Rationale

- Strategic support: Puma faced declining stock price, weakening sales, and job cuts, creating a need for strategic and revenue support—prompting Anta to step in.

- Autonomy with credibility: Puma keeps operational independence under German governance, while German business press and industry feedback view Anta as a supportive “anchor shareholder” that understands sport and is investing long term.

- Disciplined minority stake logic: The 29% position is sized to gain meaningful influence without full consolidation risk, serving as a low-risk proof of concept for deeper tie-ups later; if synergies don’t materialize or backlash emerges, Anta can exit cleanly—positioning the investor as an operational partner rather than an extractive owner.

China’s Anta Sports acquired a 29% stake in Puma for EUR 1.5B in January 2026, positioning itself as the German sportswear brand’s largest shareholder without seeking control. Puma faced declining sales (down 8% to EUR 6B through nine months of 2025) and a EUR 300M net loss, prompting 900 additional job cuts following 500 prior reductions to stem losses. This financial distress created pressing need for a strategic partner to provide capital and industry expertise.

Mutual benefits structure the partnership: Anta gains board representation and operational collaboration to leverage Puma’s global brand for Chinese market expansion, drawing on its Fila turnaround playbook. Puma stands to access Anta’s proven China expertise, demonstrated by its transformative turnaround of Fila (where China sales surged over 20x from CNY 1B in 2009 to CNY 24B by 2025) and its 2019-led consortium acquisition of Amer Sports (Salomon, Arc’teryx), which unlocked China growth via localized marketing and distribution. This pairs with Anta’s cash backing to revive Puma’s heritage brand appeal and tap into Asia’s explosive sportswear market (projected 8-10% CAGR through 2030). Puma retains operational autonomy under German governance while creating long-term value. Handelsblatt and the Frankfurter Allgemeine Zeitung (FAZ), Germany’s leading business and financial newspaper, report positive industry resonance: “Puma now has an anchor shareholder who understands sports as a strategic investor”, with corporate circles emphasising Puma’s continued independence.

Case Study 2: Chinese Investment Revives a German Supplier (Luxshare–Leoni)

Rationale

- Deal timing and salvaging value: Luxshare moved in precisely after Leoni’s attempted sale of its cable division collapsed, pushing it into distress and forcing a major restructuring — creating a rare opportunity to acquire a historically important Tier-1 supplier at a depressed valuation.

- Gaining universal OEM penetration: Acquiring one of the few European wiring-harness specialists supplying virtually all major Western automakers; Luxshare is buying instant credibility, entrenched programs, and long-cycle OEM contracts that normally take decades to secure.

- Positioning to serve Chinese OEMs entering Europe: As BYD, XPeng, and other Chinese EV players expand overseas, Luxshare gains a credibility bridge, allowing Chinese OEMs to partner with a trusted local supplier instead of building supply chains from scratch.

In September 2024, Luxshare ICT agreed to acquire 50.1% of Leoni AG, a century-old German automotive supplier of wiring harnesses and cable systems, following Leoni’s 2023 restructuring after distress triggered by a failed cable-division divestiture; the deal closed in 2025 after regulatory approvals, valuing the controlling stake at ~€320m, and also included Luxshare’s acquisition of Leoni’s Automotive Cable Solutions unit via a subsidiary.

Strategic rationale:

The transaction pairs Leoni’s entrenched OEM relationships and engineering know-how with Luxshare’s capital strength and exposure to fast-growing Chinese EV customers, positioning Leoni as a wiring-systems partner as Chinese EV OEMs expand into Europe and North America, while giving Luxshare an immediate European platform and access to Western automaker relationships that would be slow to build organically.

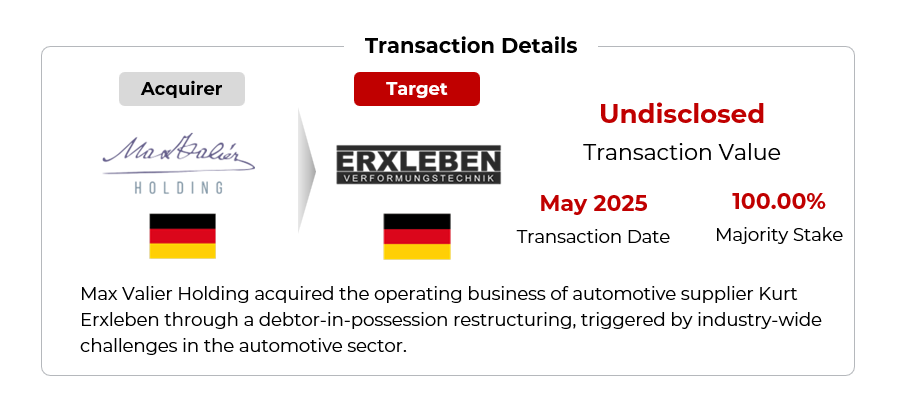

Case Study 3: Max Valier Holding fully acquired the long-standing automotive supplier Kurt Erxleben

Rationale

- Distressed acquisition: Max Valier acquired Kurt Erxleben through a debtor‑in‑possession process triggered by industry‑wide automotive pressures, enabling the rescue of a 50‑year‑old Tier‑2 supplier while preserving operations, customers, and all jobs at an attractive entry point.

- Access to differentiated technical capabilities and entrenched customer relationships: The transaction secures long‑standing expertise in complex formed, welded, and machined components, providing immediate exposure to established automotive OEM and Tier‑1 supply chains that would be difficult to replicate organically.

- PE led value creation at Kurt Erxleben: As a long‑term financial sponsor, Max Valier is positioned to apply operational expertise, disciplined capital allocation, and active ownership to modernize Kurt Erxleben and strengthen its competitive positioning.

Max Valier Holding fully acquired the business operations of Kurt Erxleben GmbH & Co. KG, a long established automotive supplier in Wildeshausen, in May 2025. The transaction followed more than a year of debtor in possession proceedings and was positioned as a continuity solution: operations continued, the brand was preserved, and all jobs were saved. Erxleben initiated debtor in possession restructuring in February 2024 amid sectorwide pressures. The company, known for complex sheet metal formed parts, welded assemblies, and machined parts for automotive and other sheet metal processing industries, was hit after a period of growth from 2020 to 2022 by a sharp decline in order volumes in 2023, compounded by higher material, labor, and energy costs. As a formed parts supplier, the company faced added strain because it could not pass these cost increases directly on to customers.

Strategic rationale:

For Max Valier, an industrial holding company that acquires and develops mid sized engineering and production businesses, the deal adds a technically capable supplier with established OEM and Tier 1 relationships. It also brings a manufacturing footprint that can be modernized as the automotive supplier market continues to change. For Kurt Erxleben, the outcome preserves the business as a going concern and is presented as the best available solution from the creditors’ perspective. More broadly, the acquisition aligns with ongoing consolidation across European suppliers.

In that sense, the Erxleben transaction echoes dynamics seen in Luxshare’s acquisition of control of Leoni. Both involve stressed European automotive suppliers using restructuring to secure a long term owner, preserve industrial capabilities, and reposition for a new competitive era. The key difference is the sponsor profile: Luxshare and Leoni illustrate an Asian strategic investor using a distressed opening to gain a European platform, whereas Max Valier and Erxleben reflect domestic or European industrial stewardship aimed at stabilizing a niche manufacturing asset and rebuilding it for sustainable growth.

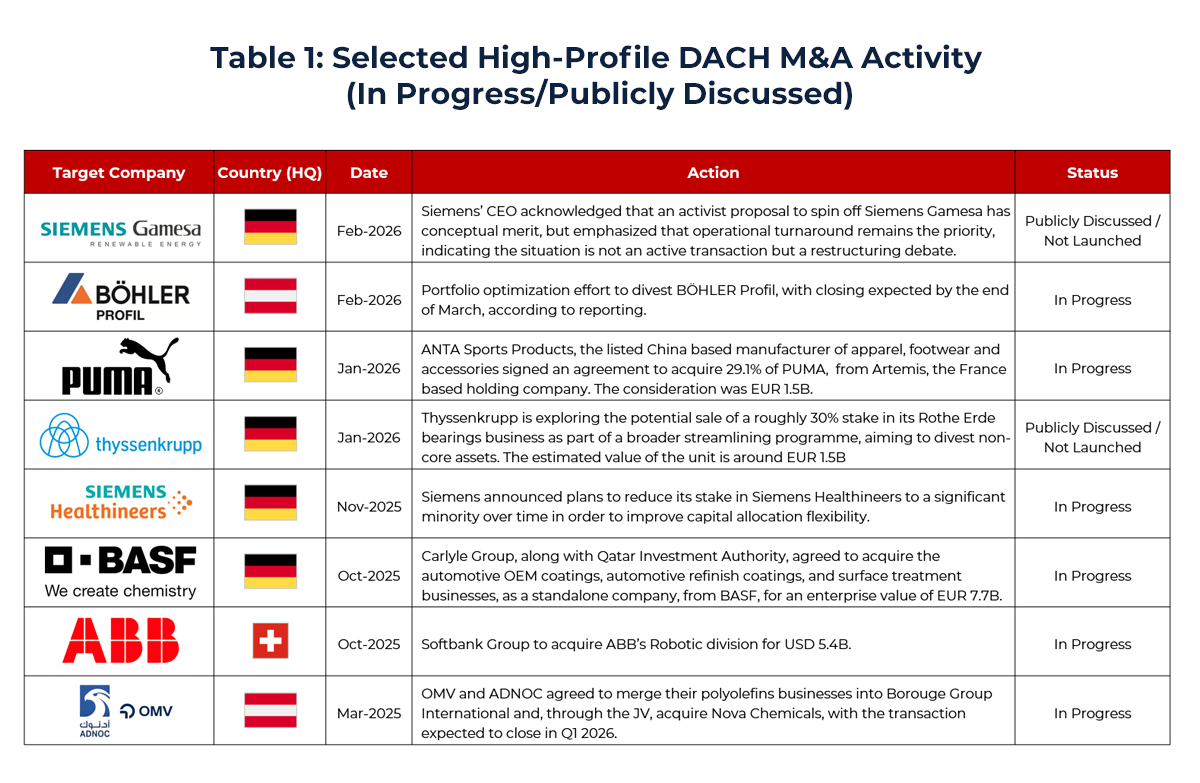

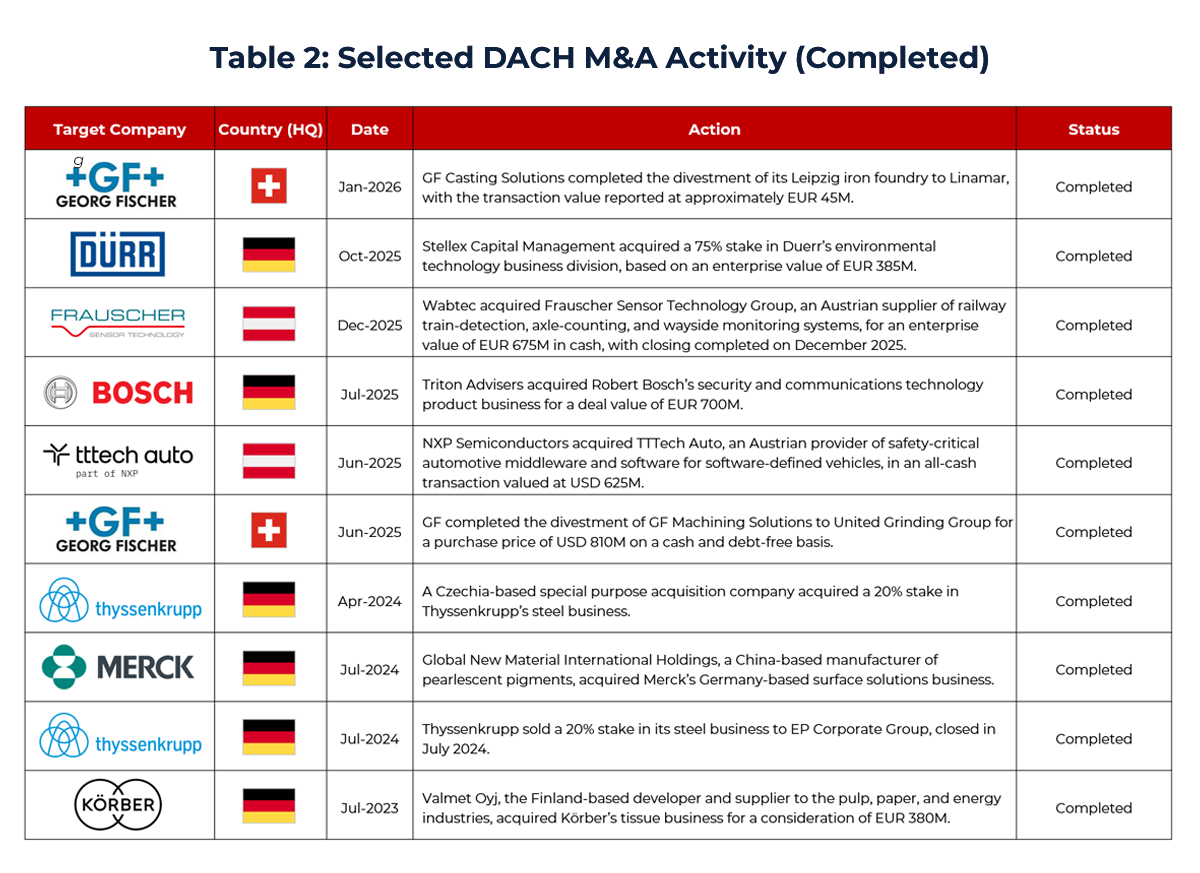

In addition to the three cases we deep-dived into, DACH industrials have seen a stir-up in M&A activity, with carve-outs and divestitures offering attractive opportunities for foreign/EU investors to access high-quality assets.

ARC has summarized the following two tables of high profile DACH industrials deals (in progress/in discussion deals vs completed).

IV. What Comes Next

Implications for 2026 and Beyond:

The DACH industrial sector is not in decline — but it is re-pricing ownership, capital, and control. The next phase of restructuring will be defined less by headline acquisitions and more by precision transactions that balance capital injection with operational continuity.

For:

- Industrial sellers: Carve-outs and minority deals offer flexibility without relinquishing identity.

- Foreign strategics: Entry is increasingly viable when aligned with long-term industrial logic.

- Financial sponsors: Structured partnerships and continuation vehicles offer differentiated access.

In Part II of this series, we will move from macro observation to deal execution: “DACH + Adjacent Europe Industrial Corridor: What to Buy and What to Sell?”

The next note will map subsectors under pressure, identify likely divestment candidates, and outline actionable entry strategies for strategics and sponsors.

Stay tuned!

References:

- Worldbank – https://data.worldbank.org/indicator/NV.IND.MANF.ZS?locations=DE

- https://www.deutsche-bank.de/ms/results-finanzwissen-fuer-unternehmen/finanzierung/11-2020-minderheitsbeteiligung-ein-helfer-in-der-krise.html#:~:text=Bei%20einem%20Mitverkaufsrecht%20hat%20ein,ihre%20Anteile%20ebenfalls%20ver%C3%A4u%C3%9Fert%20werden.

- Bundesverband der Deutschen Industrie – https://bdi.eu/themenfelder/aussenwirtschaft/auslaendische-direktinvestitionen

- https://www.pwc.de/en/deals/m-and-a-industry-trends.html

- https://www.reuters.com/business/german-corporate-bankruptcies-surge-decade-high-2025-2025-12-08/

- https://www.handelsblatt.com/unternehmen/handel-konsumgueter/sportartikel-chinas-sportriese-anta-wird-mit-milliarden-deal-groesster-puma-aktionaer/100194985.html

- https://www.faz.net/aktuell/wirtschaft/unternehmen/anta-kauft-29-prozent-puma-wird-teilweise-chinesisch-accg-200477730.html

- https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Industrial_production_statistics