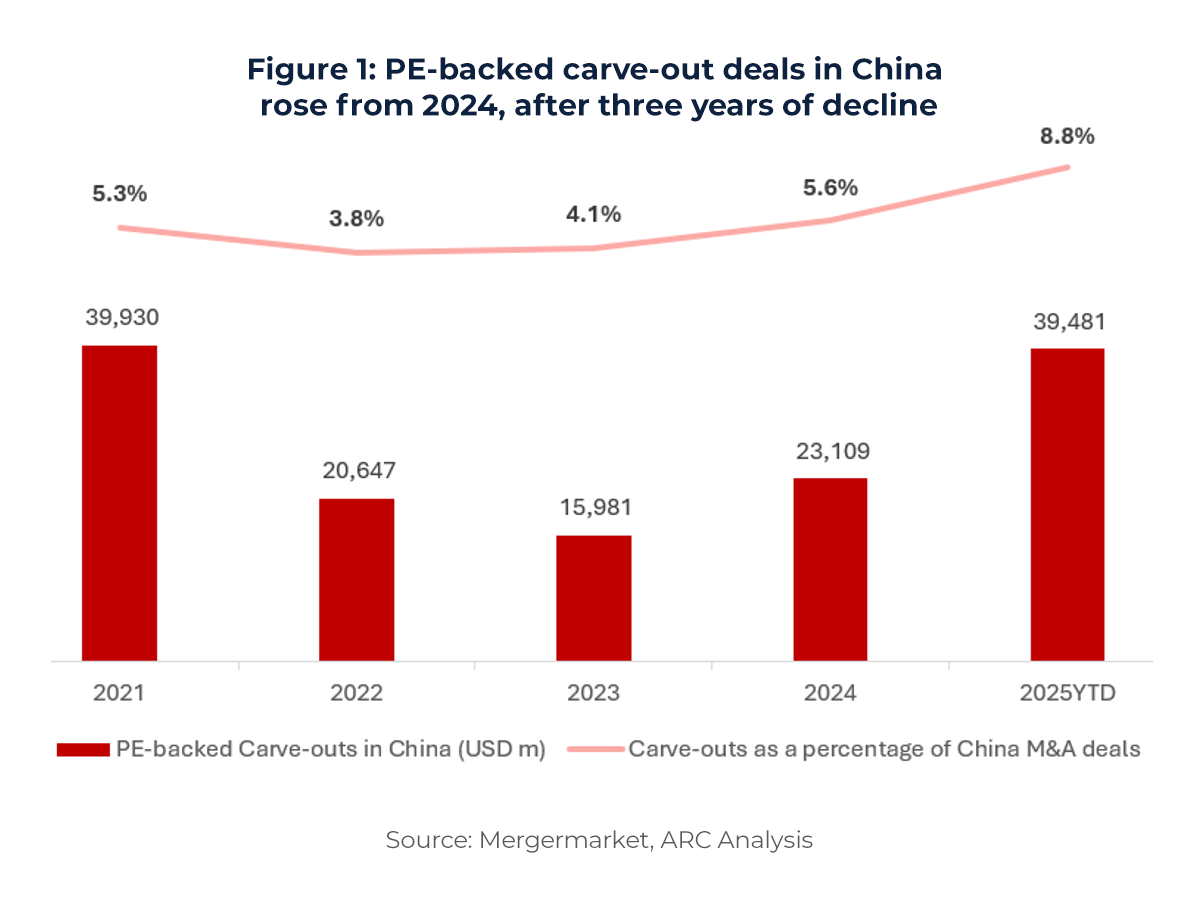

Private equity-backed carve-out deals are making a comeback in China. In 2025 year-to-date, PE-backed carve-out deals have totaled USD39bn in combined value, accounting for 8.8% of M&A deals in China. These deals span consumer and retail businesses (e.g. Starbucks’ USD4bn China joint venture, with USD2.4bn invested by Boyu Capital), logistics and real estate assets (e.g. Wanda Group’s sale of 48 shopping malls for CNY50bn, or USD6.95bn, to a PAG-led consortium), as well as data infrastructure and TMT divisions (e.g. Bain Capital’s sale of Chindata Group’s China business to Guangdong HEC-led group for USD4bn). A confluence of factors – from supportive policies and corporate deleveraging needs to multinationals re-focusing and state-owned enterprise (SOE) reforms – is driving this resurgence. Typical carve-out targets include consumer brands, retail chains, logistics arms, and data/tech units, often carved from conglomerates or foreign parents. With valuations in China resetting and buyers keen to re-capitalize, carve-outs are once again emerging as a viable path to large-scale investments.

Drivers of PE-Backed Carve-Outs in China

Policy Support and SOE Reform: Government policy is encouraging a greater role for private capital in restructuring businesses. Mixed-ownership reform initiatives have pushed SOEs to seek outside investors for non-core units, creating opportunities for PE-led carve-outs. For example, regulatory efforts to limit tech giants’ scope have prompted firms like Alibaba to consider offloading certain businesses. In addition, China’s leadership has signaled support for market-based solutions to corporate distress, which implicitly supports asset sales to financially strong investors. This policy backdrop has lowered political barriers to PE buyouts and even made local governments more receptive to private equity in traditionally state-led sectors.

Corporate Deleveraging and Distress: China’s corporate sector – especially real estate – is under pressure to reduce debt. Property developers and conglomerates facing liquidity crunches have been actively selling assets to raise cash. A prominent example is Wanda Group, whose chairman Wang Jianlin has been offloading assets to pay down debt. In 2025, Wanda sold 48 of its Wanda Plaza shopping malls to a consortium led by PAG for roughly USD7bn as part of a “property firesale” amid China’s real estate woes. This followed Wanda’s earlier sale of a 60% stake in its commercial management arm to investors led by PAG, CITIC Capital and others – a deal valued at USD8.3bn. Such distressed divestitures are expected to continue as developers and overleveraged firms shed valuable but non-core assets to stabilize their balance sheets. Beyond real estate, other indebted companies in traditional industries have likewise begun offloading quality assets to address financial challenges.

Multinationals Refocusing and Exit Pressure: Global multinationals are reassessing their China strategies amid geopolitical tensions and domestic competition. In some cases, this has led to divestiture of China operations to local buyers. Starbucks’ recent deal is emblematic: the U.S. coffee chain decided to sell a 60% stake in its China retail business to Boyu Capital for up to USD2.4bn, forming a new JV to fuel growth. This allows Starbucks to de-risk and partner with local capital for expansion, much as McDonald’s did in an earlier China carve-out. Likewise, Alibaba has been pruning its empire to refocus on core digital commerce – notably agreeing to sell its entire stake in Sun Art Retail (a hypermarket chain) to PE firm DCP Capital for USD1.3bn. These examples reflect a broader trend of foreign and domestic corporations divesting non-core or underperforming units in China. Some Western firms face shareholder pressure to exit slow-growth China segments, while Chinese tech giants under regulatory scrutiny are streamlining operations. In both cases, PE funds have seized the chance to acquire carved-out units that the original parents no longer prioritize.

SOE and Founder Transitions: Another driver is China’s ongoing economic maturation, which is producing more ownership transitions. Some founding entrepreneurs lacking successors are willing to sell controlling stakes to PE investors who can take the business to the next stage. Meanwhile, certain state-owned enterprises have been mandated to improve efficiency, leading them to spin off peripheral divisions (e.g. logistics or equipment manufacturing units) and sometimes bring in financial investors. While large-scale SOE carve-outs to PE are still nascent, policy direction suggests this could accelerate, especially in areas like infrastructure, energy, and telecom where fresh capital and expertise are needed. In sum, structural forces – from deleveraging to reform – have aligned to create a fertile environment for carve-out deals in China.

Key Deal Highlights (2024–2025)

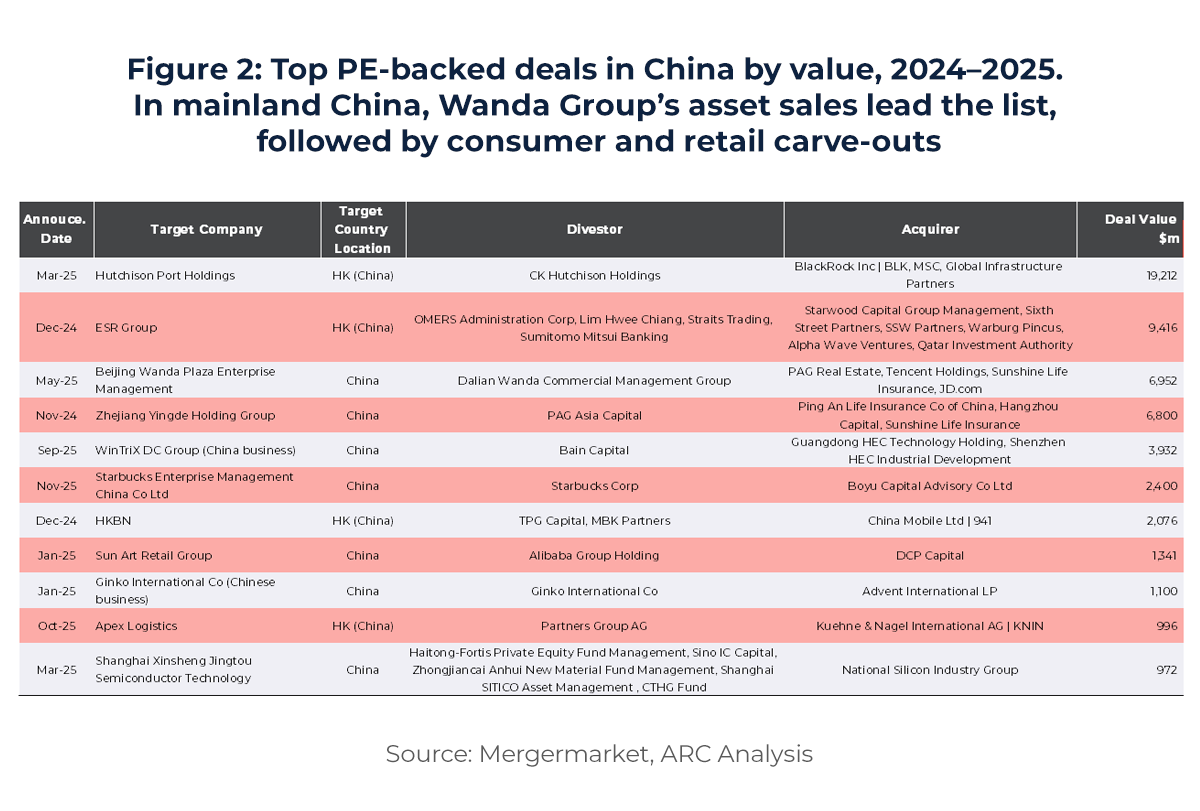

Several high-profile carve-out transactions illustrate how and where private equity is deploying capital in China’s M&A market:

- Wanda’s Mega-Deals (Real Estate/Retail): Dalian Wanda Group has been at the center of the largest recent carve-outs. In mid-2025, Wanda carved out 48 of its prime shopping malls and sold them to a consortium led by PAG (the Asian buyout firm) with partners including tech giants Tencent and JD.com and insurer Sunshine Life. The deal, structured via a fund, was worth approximately CNY50bn (≈USD7bn). This represented a bargain pickup of commercial real estate assets; the malls were sold at roughly CNY1bn each – steeply discounted from valuations a few years prior. The consortium structure is notable: PAG brought in strategic co-investors (Tencent, JD) likely to enhance the malls’ value through tenant relationships and digital integration. Wanda’s earlier deal – the sale of a 60% stake in its property management arm (Zhuhai Wanda Commercial Management) – also deserves mention. That deal, finalized in late 2023, saw PAG and fellow investors (CITIC Capital, Ares Management, ADIA and Mubadala) invest in Wanda’s mall management business, valuing the unit at USD8.3bn. These Wanda deals highlight how private equity, often teaming up with corporates or sovereign funds, is stepping in to relieve China’s debt-laden conglomerates by carving out valuable real estate operations.

- Starbucks China Carve-Out (Consumer/Retail): In November 2025, Starbucks announced it would sell a majority stake of its China business to Boyu Capital, a leading local PE firm, in a deal valuing the business at USD4bn. Boyu will invest up to USD2.4bn for 60% ownership, while Starbucks retains 40% and licenses its brand to the new venture. This carve-out is significant in both scale and structure. It marks one of the largest consumer-sector buyouts in China this year and involves a marquee global brand entrusting a domestic PE fund to operate its growth engine in China. The rationale is strategic: Starbucks gains a local partner with deep China expertise and connections, which may help it regain momentum in the face of fierce competition (e.g. Luckin Coffee). For Boyu, the attraction is an iconic brand with expansion potential – much like the 2017 McDonald’s China carve-out sold to CITIC/Carlyle consortium which delivered strong returns. Notably, M&A interest was high – more than 20 global and regional PE funds reportedly vied for Starbucks’ China arm – underscoring that investors view consumer franchises as prize targets despite recent headwinds. The Starbucks deal underscores a template for multinational carve-outs: the foreign parent retains a significant minority stake and brand control, while the PE buyer takes operational control and pledges to accelerate local growth.

- Alibaba’s Sun Art Retail Sale (Retail/Logistics): At the very end of 2024, Alibaba Group agreed to carve out and sell its entire 78.7% stake in Sun Art Retail Group, China’s largest hypermarket operator (known for RT-Mart stores), to DCP Capital. The deal was valued at USD1.3bn. This deal is a classic corporate divestiture: Alibaba is shedding brick-and-mortar retail exposure (having originally invested in Sun Art to build “new retail” synergy) to refocus on core e-commerce and technology units. DCP Capital, a China-focused PE firm, stepped in to acquire Sun Art at a significant discount to what Alibaba originally paid, indicating an opportunistic play. Alibaba expects to book a loss on the sale, but from its perspective the carve-out frees up capital and management bandwidth. For DCP, Sun Art represents a chance to turn around a nationwide retail chain; potential strategies include modernizing supply chains or integrating digital retail tech (perhaps in partnership with Alibaba or others) to boost profitability. Sun Art’s carve-out thus highlights how private equity can facilitate corporate restructuring in China by taking on non-core divisions of tech conglomerates.

Strategic Implications for Sponsors

For prospective buyers – whether global private equity funds, local PE firms, or strategic investors – China’s carve-out deals present both opportunities and challenges. Several implications emerge from the recent deal activity:

- Consortium Deals and Capital Scale: The sheer size of many carve-outs in China means that few buyers go it alone. Deals like Wanda’s USD7bn mall sale or the multi-billion Starbucks JV require substantial equity tickets, often beyond the capacity of a single fund. As a result, buyers are forming consortia or bringing in co-investors to amass the needed capital and operational expertise. These partnerships frequently blend financial and strategic players. For example, PAG’s consortium for Wanda’s malls included tech companies and insurers to not only share funding but also add operational value. Such collaborations can strengthen a bid (especially in government eyes) but also add complexity in aligning consortium interests. The ability to syndicate deals and manage partnerships has therefore become a critical skill in China’s large-cap buyouts.

- Navigating Regulatory and Political Terrain: Carve-outs in China often entail navigating a sensitive regulatory environment. Buyers must consider antitrust approvals, national security reviews (especially if the asset holds data or is in tech), and the broader political implications of acquiring a prominent Chinese business. One emerging pattern is the inclusion of state-linked capital or local investors in deals to ease approvals. Having Chinese partners (be it a state-owned fund, a local tech giant, or management rollover equity) can reassure regulators that the business will remain aligned with national interests. The Starbucks deal, for instance, handed majority control to a local firm, Boyu, which likely made the government more comfortable than a foreign buyer taking over. State-affiliated funds themselves are also directly joining buyouts – e.g., Chinese city or provincial funds are sometimes part of buyer groups – to facilitate the transaction and support policy goals. Buyers will structure deals thoughtfully, sometimes leaving minority stakes with sellers or state entities to smoothen the transaction.

- Operational Complexity and Execution Risk: Executing carve-outs is operationally challenging anywhere, and particularly so in China’s business environment. The carved-out unit often relies on the parent for certain functions – IT systems, supply chain relationships, branding, or licenses – which must be disentangled. Transition service agreements (TSAs) or long-term franchising/licensing deals (as in Starbucks’ case) are essential but can complicate the new owner’s freedom. Execution risk is therefore high: post-deal, the buyer must stand up new standalone capabilities for the business without disrupting performance. For example, integrating Sun Art Retail’s procurement and distribution with a new ecosystem after Alibaba’s exit will be a major project for DCP Capital. Similarly, ensuring continuity of Starbucks’ brand experience under new ownership will be critical for Boyu Capital. Private equity firms must have robust value creation plans and local operating expertise to handle these carve-outs – whether that means bringing in seasoned industry operators, upgrading management teams, or investing in new systems. In China, where relationships and on-the-ground know-how are key, PE firms increasingly deploy operating partners and industry specialists to manage carve-out transitions.

- Valuations and Deal Structuring: As valuations in China have corrected from prior peaks, buyers are finding more reasonable price points – but they also face earn-out and structuring considerations unique to carve-outs. Often the parent company and PE buyer will negotiate terms beyond just price, including the treatment of existing debt, retained minority stakes, or performance-based payments. Additionally, many PE-led deals in China still lean on leverage – local banks or international lenders willing to finance a portion of the buyout. Overall, dealmakers are getting creative: split payments, joint ventures, seller rollovers, and earn-outs are all tools to bridge valuation gaps and allocate risk between seller and buyer in these carve-outs.

- Local Knowledge and Talent: Finally, a strategic implication is the need for deep local knowledge. Many global PE firms have realized that to execute complex carve-outs in China, they need strong China teams or local partners. Cultural nuances, government relations, and talent management in a carved-out entity all require on-the-ground expertise. We see global funds teaming up with China-based funds or hiring seasoned Chinese executives to run acquired units. In some cases, the management team of the carved-out business is a pivotal factor: PE buyers often want to retain and incentivize key managers to ensure stability after separation. Thus, management equity rollover or option pools are common features to align interests post-deal. Buyers also must be mindful of employee perceptions – a carve-out can be unsettling to staff who suddenly have a PE firm as owner instead of a famous corporate parent. Clear communication and retention plans are part of the playbook for a successful transition.

In summary, while China’s carve-out deals offer tremendous opportunity – access to large assets at reasonable prices – investors must be adept at consortium building, government navigation, operational carve-out execution, and stakeholder management to realize the full value of these investments.

Outlook for 2025–2026

The outlook for PE-backed carve-outs in China over the next 18–24 months is optimistic. Deal pipeline and momentum suggest that 2025 could mark a multi-year high in buyout activity. As of late 2025, private equity acquisitions of Chinese companies had already reached USD25bn for the year, exceeding 2024’s total and on track for the highest level since 2021. This upswing in activity is expected to carry into 2026, barring any major macroeconomic or political shocks. Several trends underpin this positive outlook:

- Continued Corporate Restructuring: China’s economic landscape in 2024–2025 – characterized by slower growth, sectoral downturns (property, etc.), and tech industry shifts – has only increased the pressure on firms to restructure. We anticipate more motivated sellers, both foreign and domestic. For instance, other global consumer companies may emulate Starbucks and McDonald’s by divesting China units if they find local partners willing to invest (recent rumors in consumer goods and healthcare point in this direction). Likewise, Chinese conglomerates and tech giants under regulatory or financial strain will likely continue pruning their portfolios. Alibaba’s ongoing reorganization into separate business units could spawn further carve-outs (its supermarket chain Freshippo, for example, has been rumored as a carve-out candidate if an IPO doesn’t materialize). The pipeline of potential deals includes everything from food and beverage brands to industrial and manufacturing subsidiaries of larger state firms. Industry insiders suggest that several sizable deals in healthcare and consumer sectors are in advanced planning, often involving local PE firms teaming up with “local champions” to take over assets. This model of domestic consortium buyouts is likely to be a hallmark of upcoming deals.

- Improving Investor Sentiment: After a cautious period, global investors are tentatively warming back up to China. Valuations have come down to more attractive levels, and some of the regulatory uncertainties have begun to clear. Top PE fund executives note that many international LPs feel over-allocated to U.S. assets and are looking to rebalance towards Asia, with China being a key beneficiary if risks are manageable. Throughout 2025, heavyweight funds like Warburg Pincus, KKR, Blackstone, and others have publicly indicated interest in new deals in China – a notable shift from the “wait-and-see” stance a few years prior. This does not mean indiscriminate optimism, but for well-structured carve-outs in resilient sectors, the buyer pool is growing. We expect more participation from pan-Asian private equity funds, sovereign wealth funds from the Middle East, and even North American pensions, often in partnership with local Chinese funds. The recent success of deals like the Starbucks JV (attracting numerous bidders) has sent a signal that deals can get done and deliver value, which in turn should encourage more activity. In short, the frost of investor hesitancy is thawing, and 2025–2026 should see increasing capital flow into Chinese control deals.

- Sectoral Hotspots: Based on current deal flow and China’s strategic priorities, consumer, healthcare, and technology/data infrastructure are poised to be hotspots for carve-outs. Consumer and retail will remain active – China’s enormous market and changing demographics create both challenges and opportunities, and we expect to see carve-outs of both foreign consumer brands (seeking local partners) and domestic consumer companies (seeking growth capital or exits). Healthcare is emerging as a key area: with China’s healthcare reforms and local champions rising, multinationals might spin off China divisions (e.g. in medical devices or pharma) to local investors, and some indebted Chinese hospital groups or pharma distributors could sell stakes to PE for restructuring. Technology and data infrastructure deals are also likely – the government is balancing national security with the need to let private capital fund innovation. We might see carve-outs in sub-sectors like cloud computing, fintech, or semiconductors where big tech firms or conglomerates divest minority stakes to outside investors. Additionally, logistics and supply chain assets (warehousing, distribution, transportation) remain very much on the radar, given China’s push for efficiency in this space – further separation of logistics arms from e-commerce firms (akin to JD Logistics’ earlier carve-out) could happen if market conditions favor it.

Several carve-out transactions currently under discussion could further shape the 2026 landscape. Restaurant Brands International signed a definitive agreement in late 2025 to transfer 83% of Burger King’s China operations to a CPE-led joint venture, in a USD350mn transaction aimed at accelerating store growth (Reuters, Nov 2025). TianTu Capital is exiting its stake in Yoplait’s China business to IDG Capital in a deal valuing the brand at approximately CNY1.8bn (36Kr, Dec 2025). Domino’s U.S. parent has continued to reduce its stake in listed franchisee DPC Dash via block trades, reflecting a longer-term shift in franchisor exposure (QSR Media Asia, May 2024). Meanwhile, GE HealthCare is reportedly exploring strategic options for its China operations, including a potential stake sale, with discussions said to be in early stages (Reuters, Sept 2025). These transactions underscore the continued appetite for partial or full carve-outs in China’s consumer and healthcare verticals, especially as multinationals and local funds reconfigure partnership models.

- Execution and Government Oversight: On the flip side, the pace of carve-outs will also depend on execution and regulatory approval timelines. Chinese authorities will likely scrutinize deals that involve sensitive assets or large layoffs, meaning buyers must present carve-outs as growth and value-enhancing for the economy. The government’s recent stance has been cautiously supportive – encouraging private investment to revitalize the economy – so long as it doesn’t lead to asset stripping or social instability. As such, responsible dealmaking is crucial. We expect deal structures in 2025–2026 to include commitments to invest in the business, retain employees, and align with national goals (e.g. digitalization, rural consumption, “common prosperity” initiatives) to win government buy-in. State capital will continue to co-invest where appropriate. Local governments, facing fiscal pressure, may also proactively facilitate carve-outs of projects and companies under their purview to raise funds – for example, privatizing certain infrastructure projects or selling stakes in local SOE subsidiaries to PE consortia. These developments could add to deal volume, though they tend to be complex and time-consuming.

In conclusion, the resurgence of PE-backed carve-outs in China appears set to continue into 2025 and 2026. The driving forces – corporate restructurings, policy tailwinds, and investor interest – are all aligning. China’s M&A market is shifting from predominantly minority growth investments toward more control-oriented buyouts, of which carve-outs are a major component. While risks remain (macroeconomic uncertainty, geopolitical tensions, execution hurdles), the recent successes have created a blueprint for how to navigate them. We expect a steady flow of landmark deals in the coming years, as professional investors and strategic players partner to unlock value from corporate China’s vast portfolio of assets. For investors and strategics prepared to handle the complexity, China’s carve-out arena offers compelling opportunities – a chance to acquire strong businesses at reasonable prices and to shape their future outside the shadow of former parents. If the momentum holds, 2025–2026 could very well cement China’s arrival as a major market for large-scale buyouts and carve-outs, reshaping the country’s corporate landscape in the process.

The financial figures and transaction details presented in this article are derived from publicly available sources, including press releases and media reports. As such, they are intended for illustrative and educational purposes only and may not fully reflect the actual deal structure, terms, or confidential elements of the transaction. Readers should not rely solely on this information for investment, legal, or financial decision-making.

Author:

Simon Lou

Associate

References:

- Mergermarket: Deal Search

- Reuters. (2025) “Starbucks brews a murky China infusion”

- Reuters. (2025) “Wanda lights up China’s great property firesale”

- Reuters. (2025) “Global private equity funds consider return to China as investors pivot from US”

- ION Analytics. (2024) “China buyouts: Investors expect structural change to drive control deals”

- SCMP. (2025) “Alibaba sells hypermarket operator Sun Art for US$1.7 billion to refocus on e-commerce”

- ION Analytics. (2025) “PE must evolve to exploit Asia’s growing large-cap buyout market”